In 2025, Vietnam’s beauty market is entering a new growth phase, driven by changes in how consumers approach and sustain personal care habits. Alongside the advantages of a young population and the rapid expansion of e-commerce, consumer behavior increasingly reflects the role of beauty as part of everyday life. Amid intensifying competition between domestic and international brands, Vietnam is emerging as a key market in Southeast Asia, marked by the intersection of beauty, technology, and evolving consumer culture.Within the skincare category, growth momentum is shifting away from intensive treatments and multi-step routines toward the need to maintain stable skin conditions that fit into daily lifestyles. This shift is also evident in social media discussions, where skincare is increasingly perceived as a long-term living habit rather than a short-term beauty solution.Buzzmetrics’ report Vietnam Facial Skincare – Market Shifts & Evolving Consumer Demands (2024–2025) analyzes more than 61 million skincare-related discussions collected between October 1, 2024 and September 30, 2025. The report highlights how consumers’ perceptions, product choices, and usage behaviors have evolved compared to previous years.

This article focuses on three key areas:

→ To explore the full dataset, detailed insights by skincare needs, and how brands can leverage these signals in their strategies, please refer to the Vietnam Facial Skincare – Market Shifts & Evolving Consumer Demands 2024–2025 – Full Report.

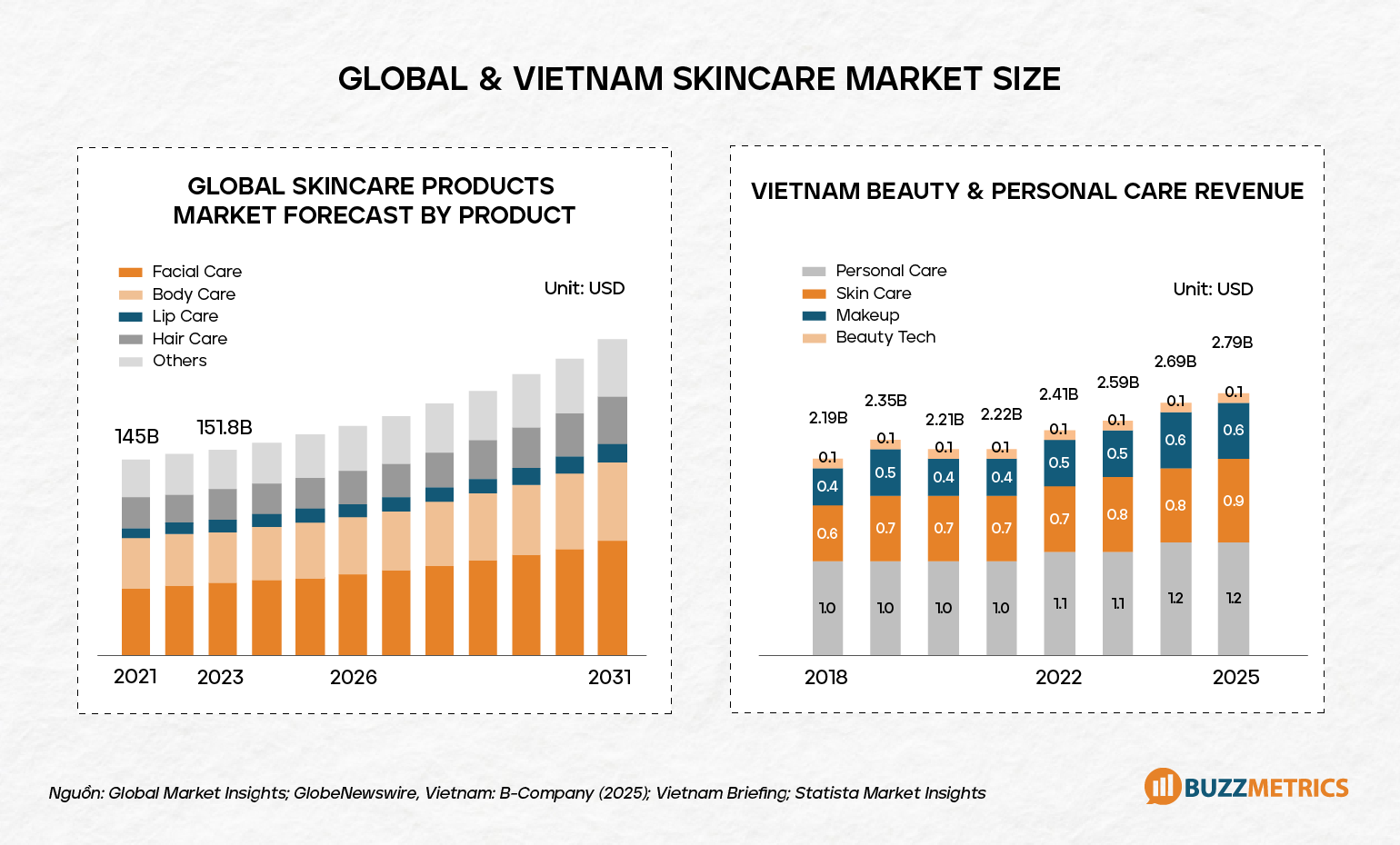

Globally, skincare remains one of the most stable growth segments within the beauty industry, reaching USD 151.8 billion in 2023 and projected to grow to USD 231.6 billion by 2032 (CAGR ~5%). However, the key shift lies in the nature of demand: growth is no longer driven by adding more steps to skincare routines, but by how consumers approach skincare as a long-term process of maintaining skin health.

In Vietnam, the Beauty & Personal Care market is estimated at approximately USD 2.74 billion, with a steady growth rate of around 3.3% annually through 2029. Within this landscape, skincare continues to be a core growth driver, fueled by daily skincare habits and rising demand for gentle, skin-friendly formulations that are easy to maintain in simple routines. The expansion of e-commerce and social commerce has further accelerated this trend, enabling consumers to access information, compare products, and reference real user experiences before making purchase and usage decisions.

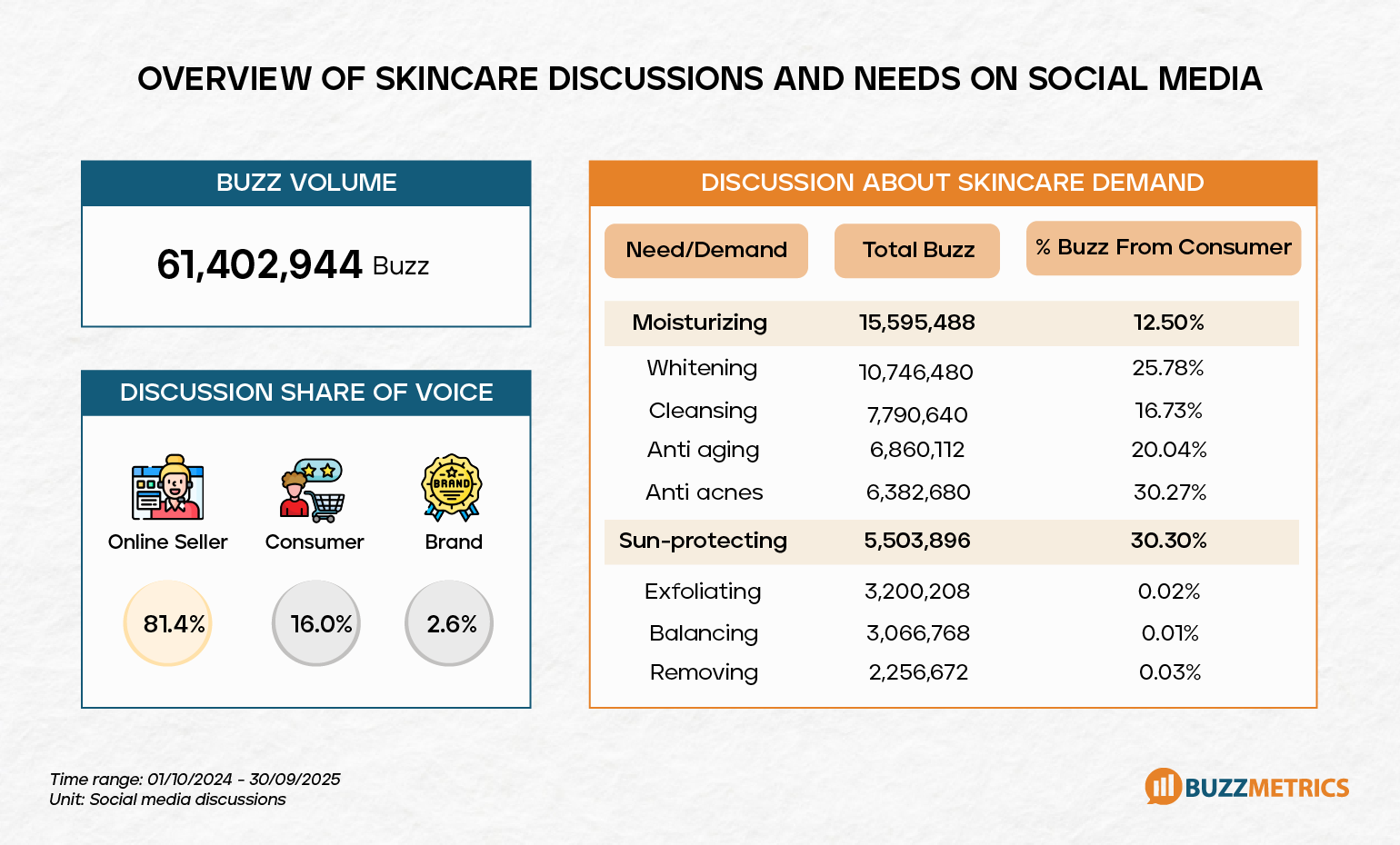

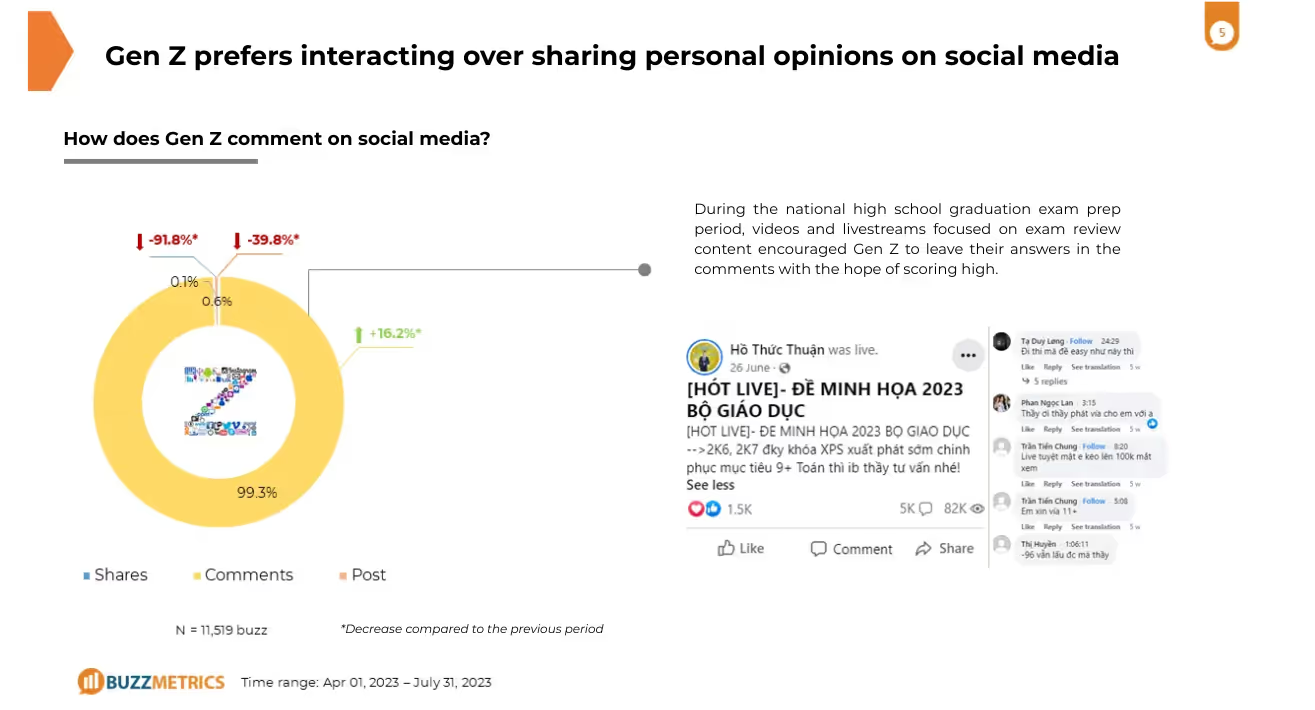

With over 61.4 million discussions during the research period, skincare remains one of the most active categories on social media. The majority of content is generated by online sellers (81.4%), while consumer- and brand-driven discussions account for a smaller share. This indicates that while social skincare content is heavily sales-oriented, it does not fully reflect how real consumer needs are formed.

When focusing specifically on discussions led by consumers, key themes revolve around on-skin feel, comfort during use, and the ability to sustain skincare routines over time. Foundational steps such as moisturizing and sun-protecting are mentioned more frequently than intensive corrective needs. This suggests that consumers increasingly view skincare as a daily habit, where consistency and stability matter more than immediate results.

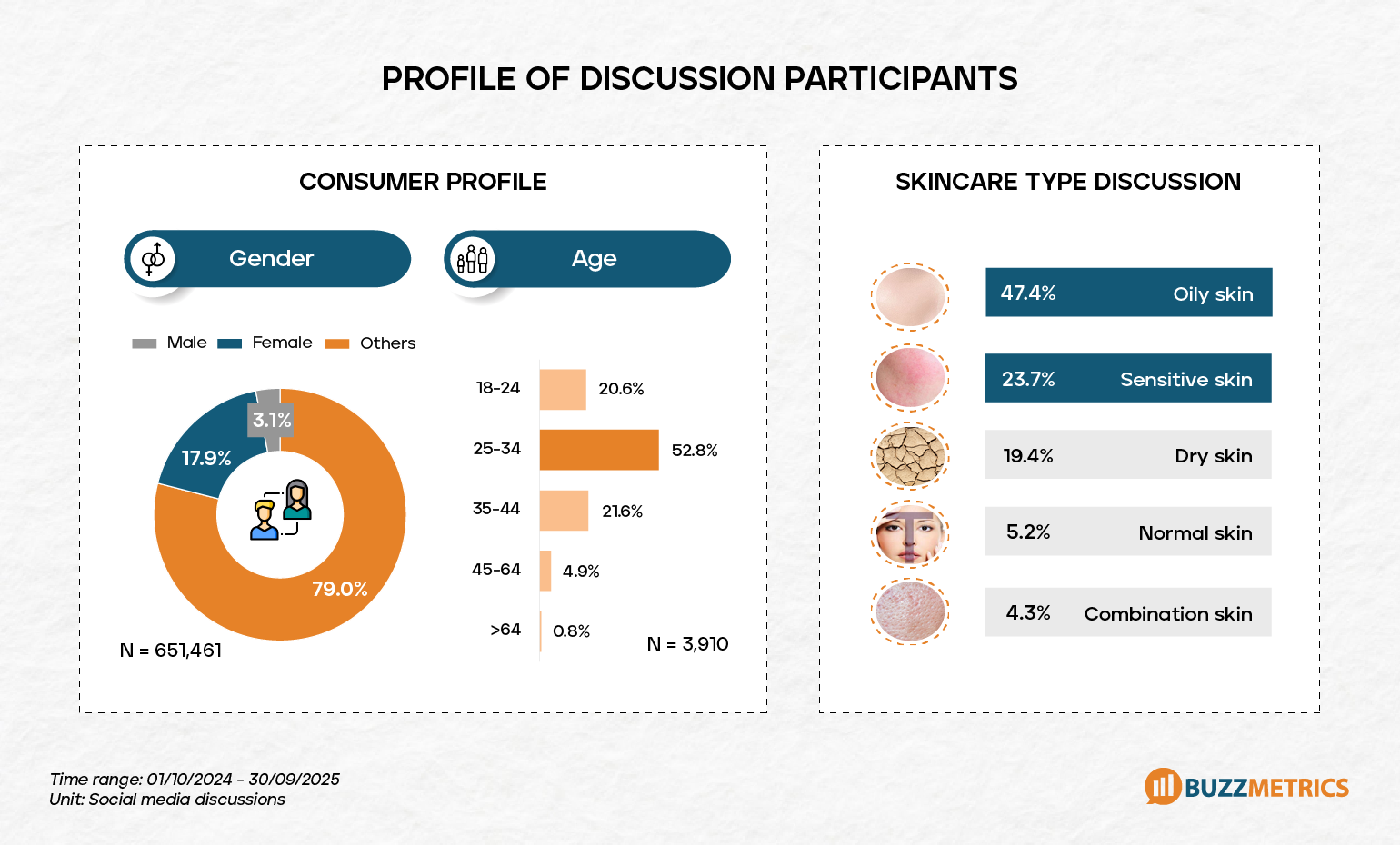

Current skincare discussions are dominated by young female users, particularly those aged 25–34, a group with strong purchasing power and high social media engagement. For this segment, skincare is no longer about experimenting with trends, but has become an integral part of daily life. Their conversations emphasize routine stability, product suitability, and the experience of regular use.

At the same time, the growing participation of male users indicates that skincare is expanding beyond traditional beauty boundaries. This group tends to approach skincare pragmatically, prioritizing simplicity, convenience, and comfort.

By skin condition, oily skin (47.4%) and sensitive skin (23.7%) are the most frequently mentioned. In the context of Vietnam’s hot and humid climate and urban environment, this highlights clear product expectations: gentle formulations, low risk of irritation, and suitability for long-term use. Rather than seeking aggressive solutions to “fix” skin issues, consumers increasingly talk about preventing deterioration - avoiding irritation, minimizing congestion, and maintaining comfort with continuous use.

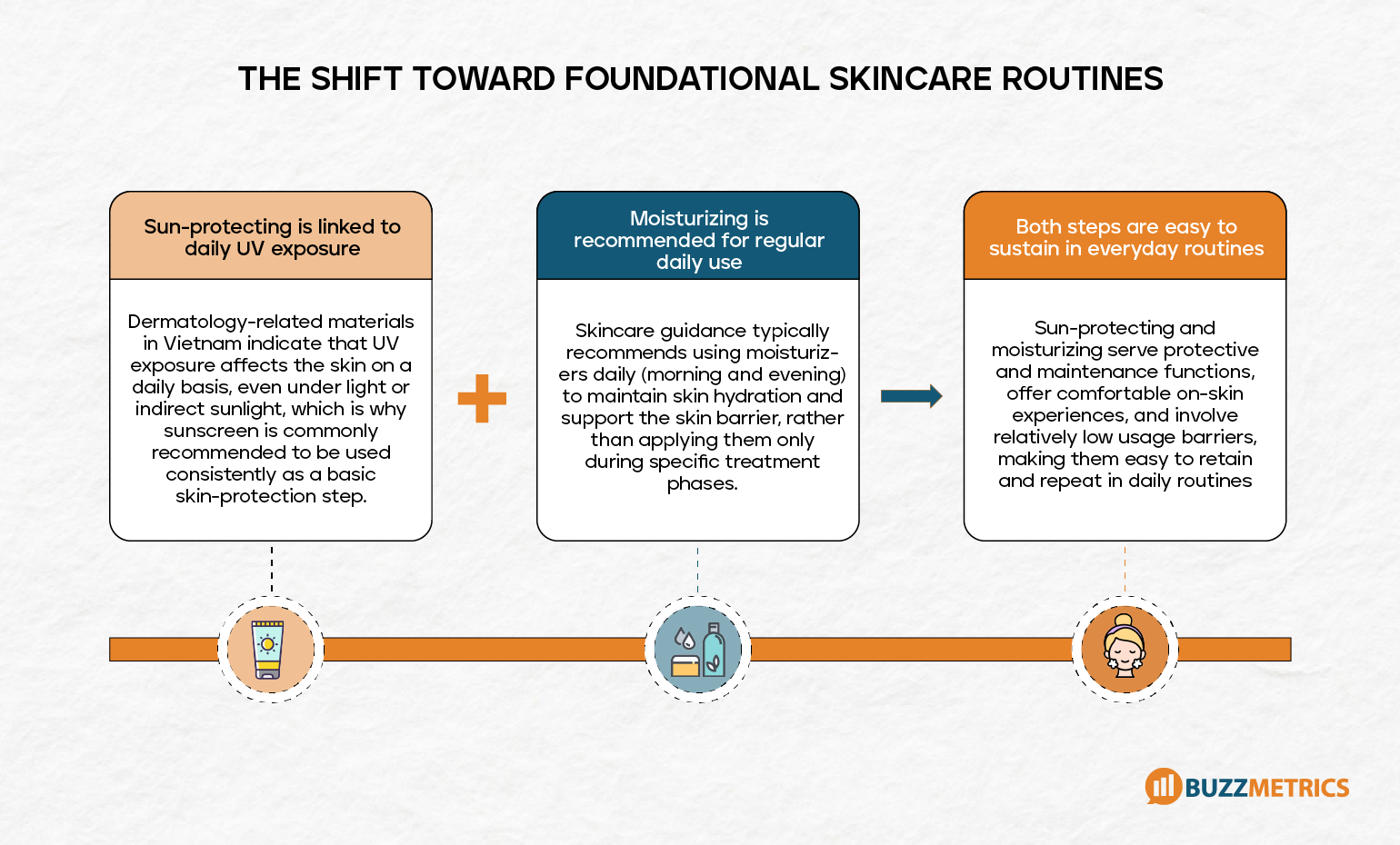

Social media discussions indicate that skincare demand is increasingly centered on foundational routines that can be sustained daily. Consumers favor steps that are easy to repeat, comfortable to use, and effective in maintaining stable skin conditions over time. Within this context, sun-protecting and moisturizing consistently appear as core elements of daily routines, closely linked to living conditions in Vietnam and dermatological recommendations for protecting and maintaining the skin barrier.

Sun-protecting is viewed as a basic defensive step, while moisturizing supports skin stability amid constant exposure to heat, humidity, pollution, and external stressors. What both steps share is a low usage barrier, allowing them to be easily integrated and consistently maintained without placing additional pressure on the skin.

However, across both product categories, consumers continue to hold high expectations for a balance between effectiveness and user experience. Products are expected to deliver functional benefits while remaining lightweight, comfortable, and safe for everyday use. Finding options that can support long-term commitment remains a challenge.

This shift presents new requirements for brand strategies and product portfolios. The focus is moving away from short-term efficacy toward the ability to accompany consumers in their daily lives. Understanding emerging needs on social media, along with unmet expectations and usage barriers, becomes a critical foundation for informed brand decision-making in the next phase of growth.

By synthesizing market data and social media discussions, several signals are clearly reshaping how consumers approach skincare:

_11zon.webp)

Matcha has become a global beverage phenomenon in recent years, even leading to shortages in Japan (according to Thanh Nien Newspaper). In Vietnam, the matcha market size is forecasted by Mobility Foresights to grow from USD 340 million in 2025 to USD 500 or even USD 780 million by 2030. Furthermore, according to IPOS, consumers are willing to pay an extra VND 10,000 - 20,000 for a high-quality cup of matcha. So, how is matcha being discussed on social media?

Buzzmetrics' report, based on an analysis of 3.78 million social media discussions, will focus on answering two questions:

In recent years, social media has witnessed the rise of many "trendy" food and beverages such as scallion milk tea, hand-squeezed lemon tea, cheese coin bread,... However, these products only received attention for a relatively short period and almost disappeared after just one or two months. In contrast, there are foods and beverages that are seasonal, receiving much attention on special occasions, such as mooncakes for the Mid-Autumn Festival or red bean sweet soup for the Double Seventh Festival. And there are also sustainable items, always of interest to users at any time, like coffee or milk tea. So, which category does Matcha belong to?

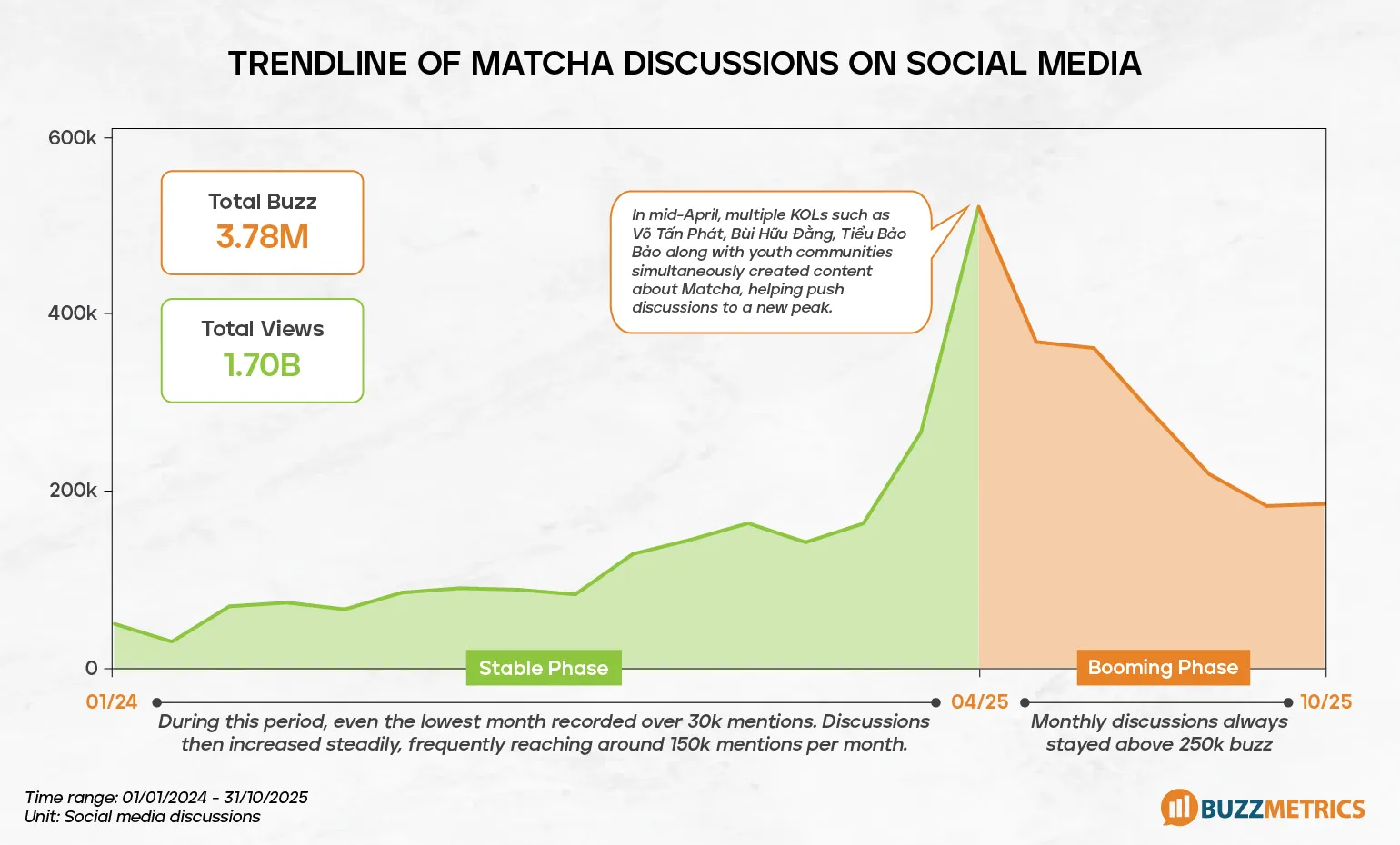

From Buzzmetrics' data, in the period from early 2024 to October 2025, the total volume of discussions about Matcha reached nearly 3.78 million buzzes. In April 2025, discussions about Matcha increased sharply. This stemmed from the simultaneous participation of many KOLs and young community pages with a series of humorous content about Matcha. The sudden spike in discussions in April led many to easily associate Matcha with the "one-hit wonder" model – a rapid explosion followed by a quick cooling down. However, upon more detailed examination, the matter is not that simple.

Before April 2025, Matcha had been continuously discussed since early 2024, with the lowest level still reaching about 30,000 discussions per month. Moving into the second half of 2024 and throughout 2025, monthly discussions maintained above 100,000, even exceeding 150,000 discussions in many months. After April, Matcha did not disappear from the discussion flow but returned to a stable state, being mentioned consistently and regularly. This shows that the sudden increase in April was just an "outlier" amplifying a topic that users were already interested in beforehand.

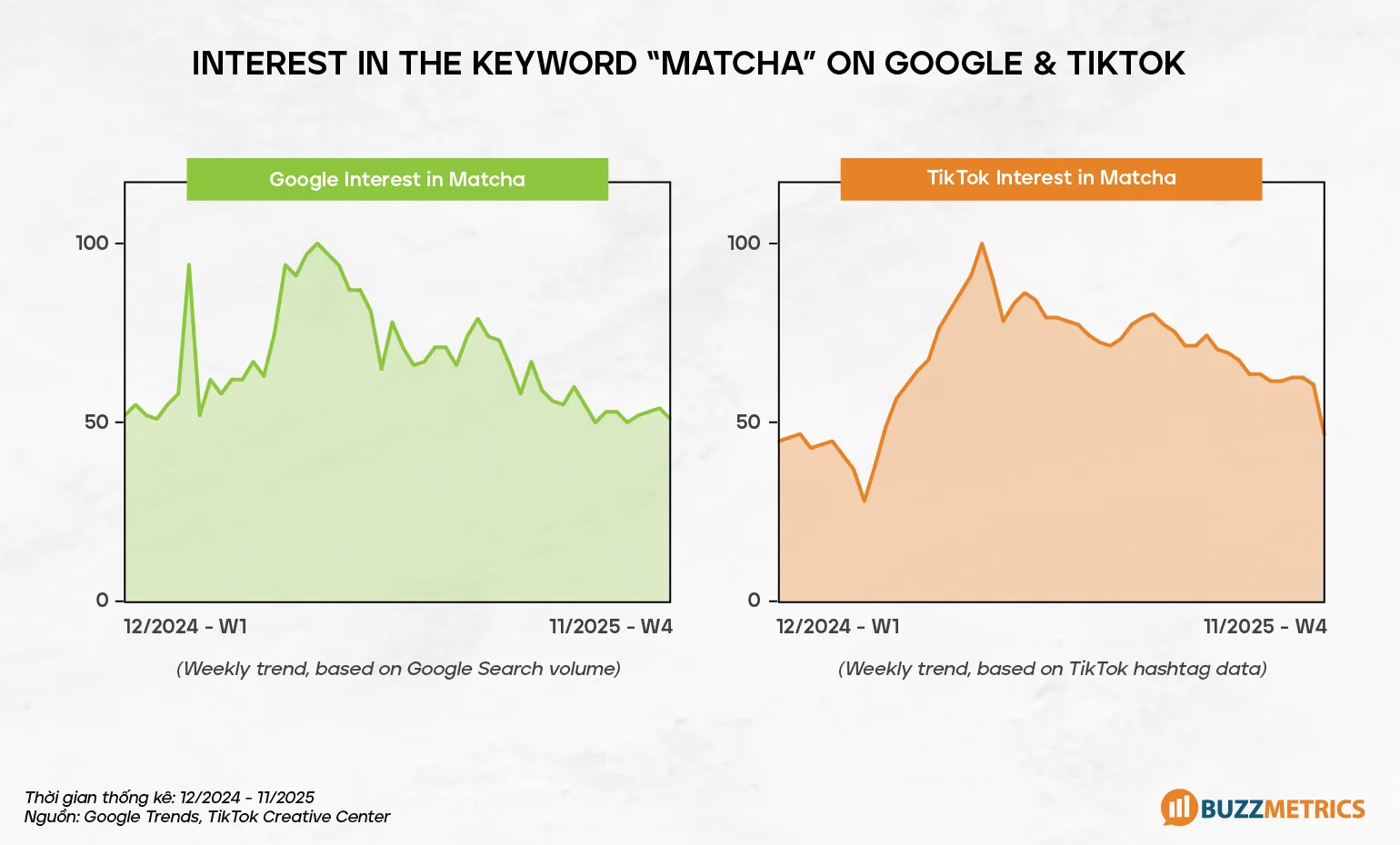

The data provided by Google and TikTok will help to more specifically visualize user interest in Matcha. According to Google Trends, searches for Matcha in Vietnam were relatively volatile from late 2024 to early 2025, peaking also around April 2025 and then stabilizing with an interest index always above 50 each month. TikTok measurement based on hashtags about Matcha also shows a similar development.

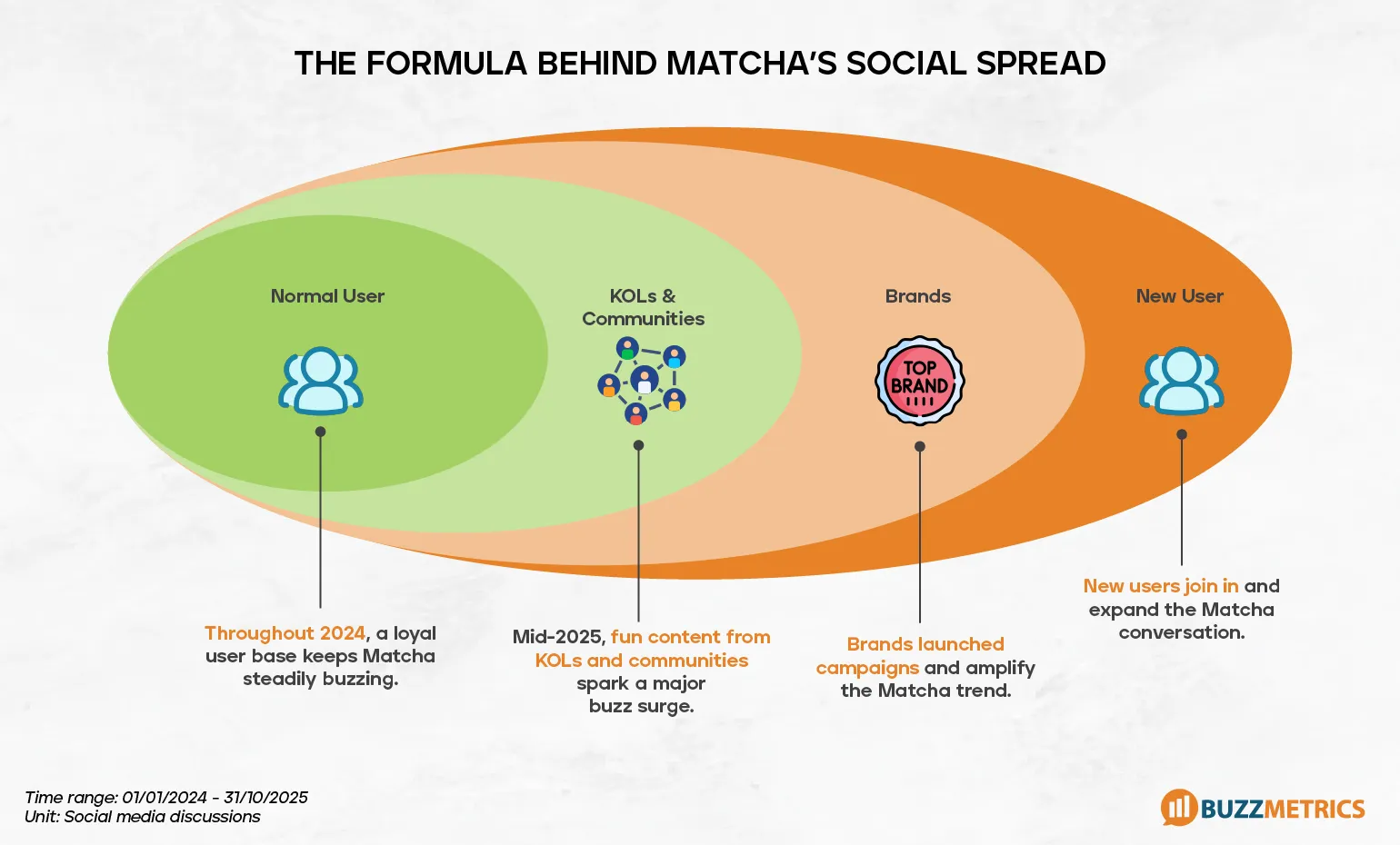

Overall, Matcha shifted from a topic discussed steadily on social media to a prominent trend thanks to multi-layered viral effects. This process occurs through four steps:

(1) It started with a group of users who liked drinking Matcha and discussing Matcha on social media.

(2) KOLs and community pages began paying attention to Matcha and participating in the content creation process, helping to amplify discussions. At this point, Matcha was already being widely discussed across all social media platforms, with Facebook and TikTok leading.

(3) Brands recognized Matcha's potential so they launched responsive products, promoting and extending the level of spread.

(4) New users from different age groups joined the discussion. The Matcha topic was expanded and maintained over time.

Also according to Buzzmetrics' statistics in November 2025, Matcha is the third most discussed non-alcoholic beverage, only after milk tea and coffee. Thus, overall, Matcha does not operate as a short-term trend, but has become a sustainable trend, driven by actual demand and consumer behavior. So what has created its widespread appeal and made users stick with Matcha long-term?

To understand why Matcha can maintain long-term appeal, we need to look at the real motivation behind user behavior. Discussion data shows that consumers come to Matcha not only out of curiosity or following the trend.

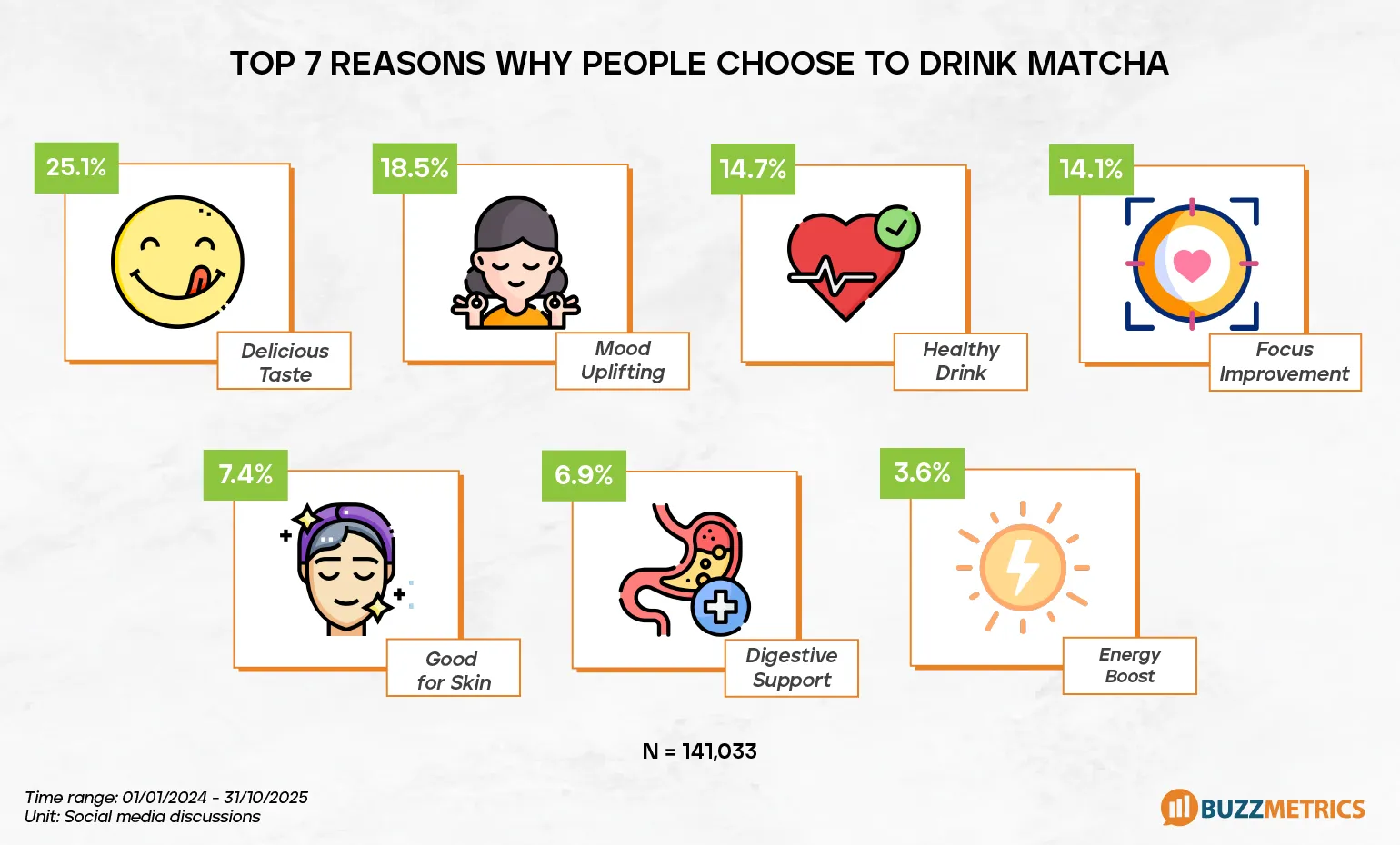

Firstly, Matcha is loved because it meets many consumer needs simultaneously. There are 7 main reasons users choose to drink Matcha regularly that are discussed. Prominent among them are its easy-to-drink flavor, relaxing feeling – improving mood, stable energy source, along with benefits related to health and mentality.

Compared to other caffeinated beverages, Matcha is evaluated by users as providing a gentle feeling of alertness, not causing "irritability," suitable for regular use throughout the day. This is also the reason Matcha appears densely in discussions associated with healthy lifestyles, effective work, and self-care – topics of increasing interest on social media.

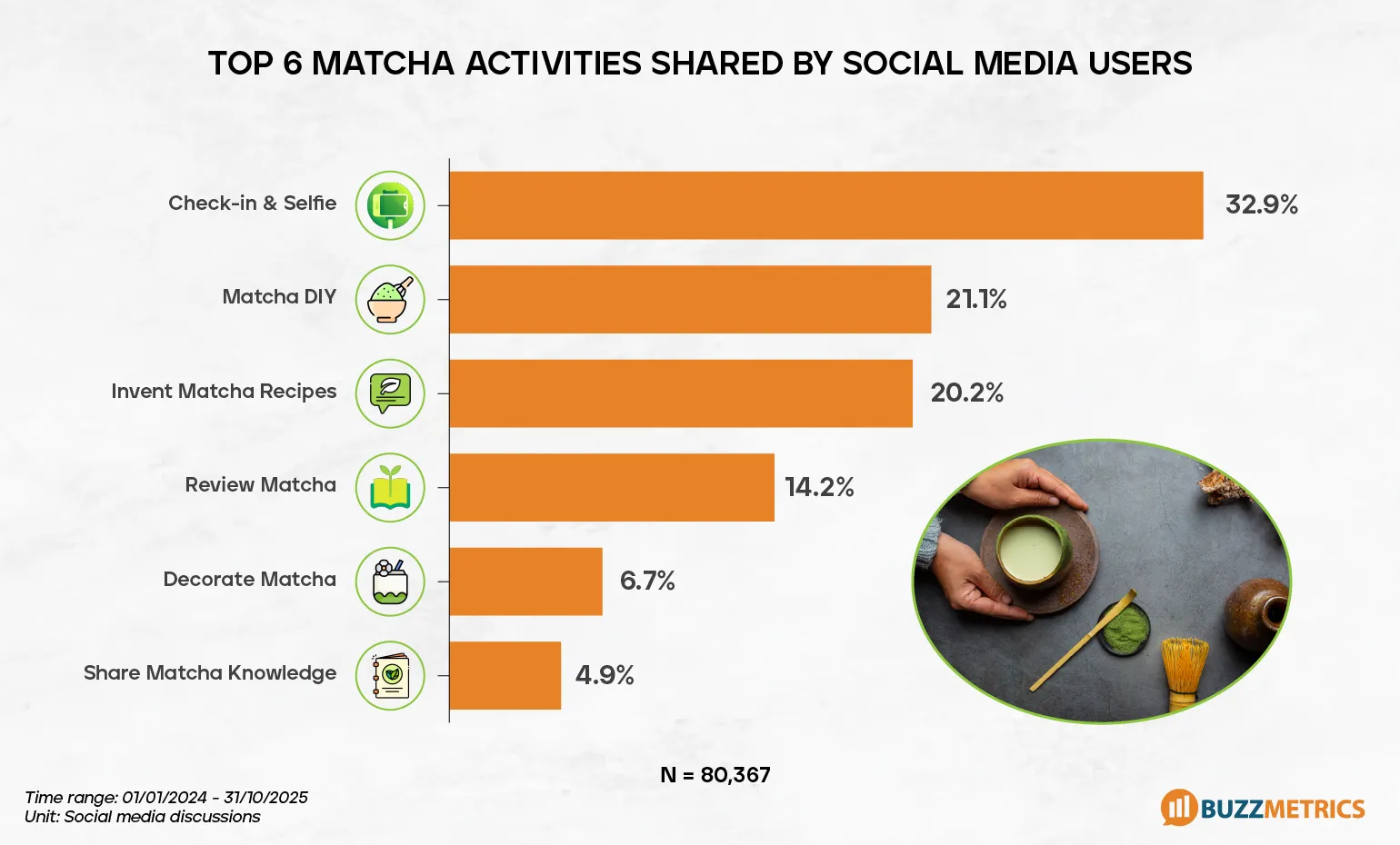

Not stopping at just drinking, Matcha is also mentioned in various user activities. Data shows that discussions about Matcha range from drink check-ins, knowledge sharing, product reviews, to entertainment and lifestyle content. This transforms Matcha from a mere consumer product into a highly personalized experience.

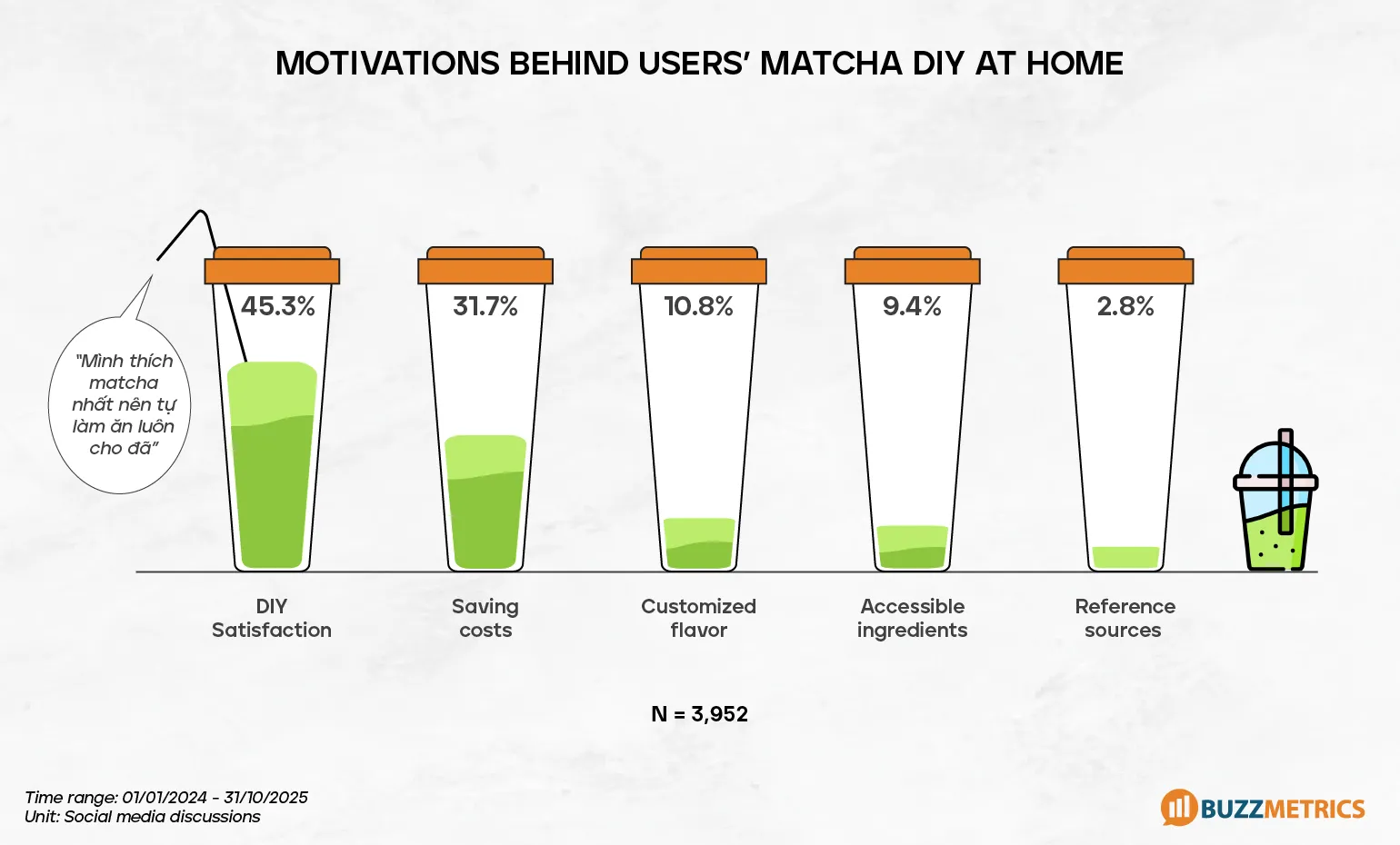

In particular, the DIY Matcha trend clearly reflects the role of Matcha in daily life. Making Matcha at home not only helps save costs but also brings a feeling of relaxation, creativity, and proactivity. Accessible ingredients, not overly complicated preparation methods, and the ability to customize flavor make Matcha a true "hobby" for many users.

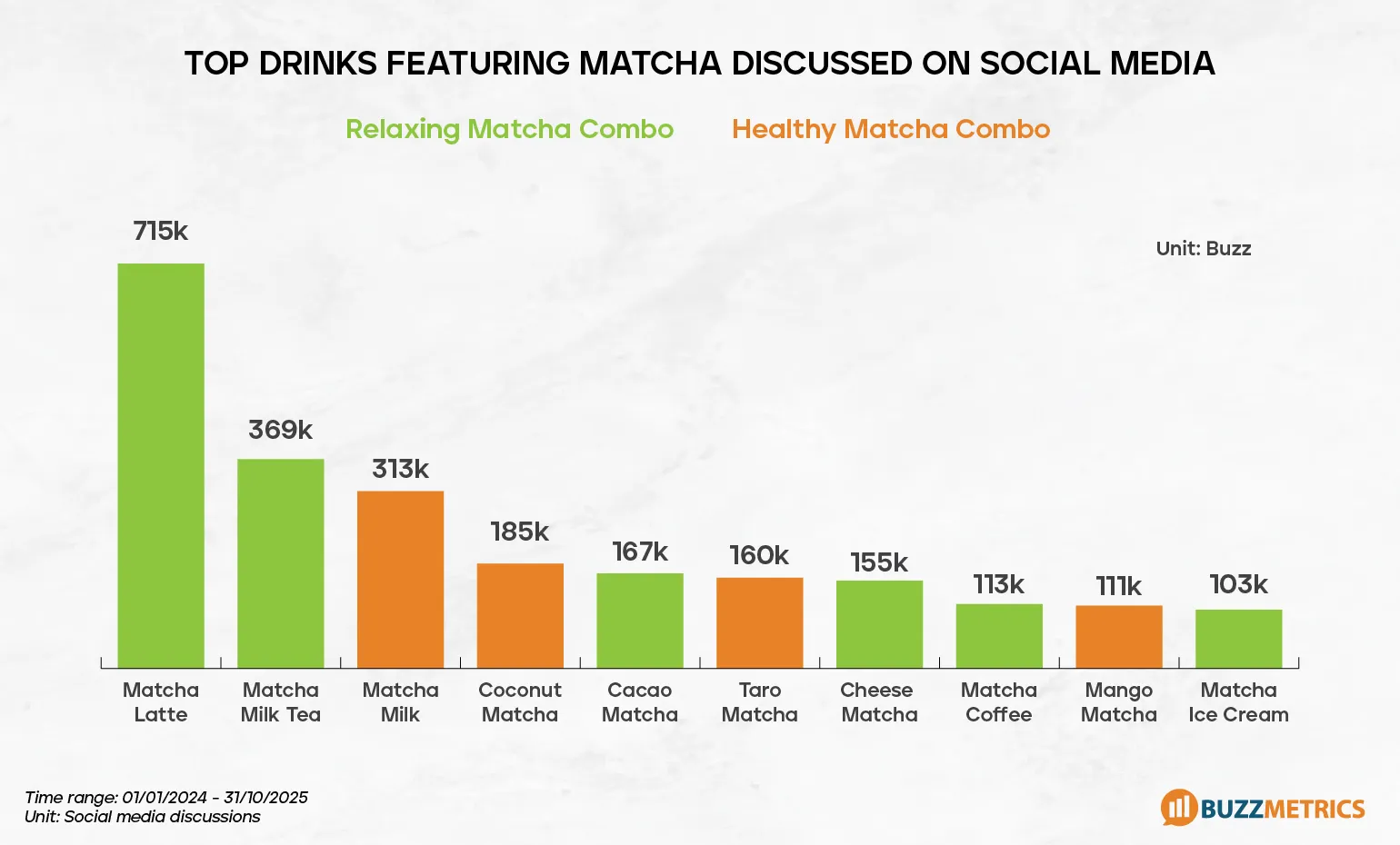

The flexibility of Matcha is also shown in its ability to combine with many different beverages. Matcha can be paired with fruits like mango, taro, coconut to bring a drink that is both delicious and "healthy"; on the other hand, it can be combined with milk tea, coffee, ice cream to offer a youthful drink, exuding Gen Z style. This very "adaptability" helps Matcha continuously refresh its flavor, avoid boredom, and maintain sustainable discussion on social media.

In summary, Matcha has crossed the boundary of a short-term trend to become a sustainable beverage trend. This is demonstrated by the fact that topics surrounding Matcha have always been stably discussed for nearly two years.

More importantly, consumers choose Matcha not because they are following the crowd or FOMO (fear of missing out). Users stick with Matcha because of the tangible value and positive emotions it brings: From its distinctive flavor, the joy in self-preparation, to the feeling of improving mood and being beneficial for health. They are not just buying a drink, but are investing in a personalized experience and a more proactive, joyful, and healthy lifestyle.

This is the foundation that helps Matcha continue to have a solid position on social media and in the long-term strategy of F&B brands.

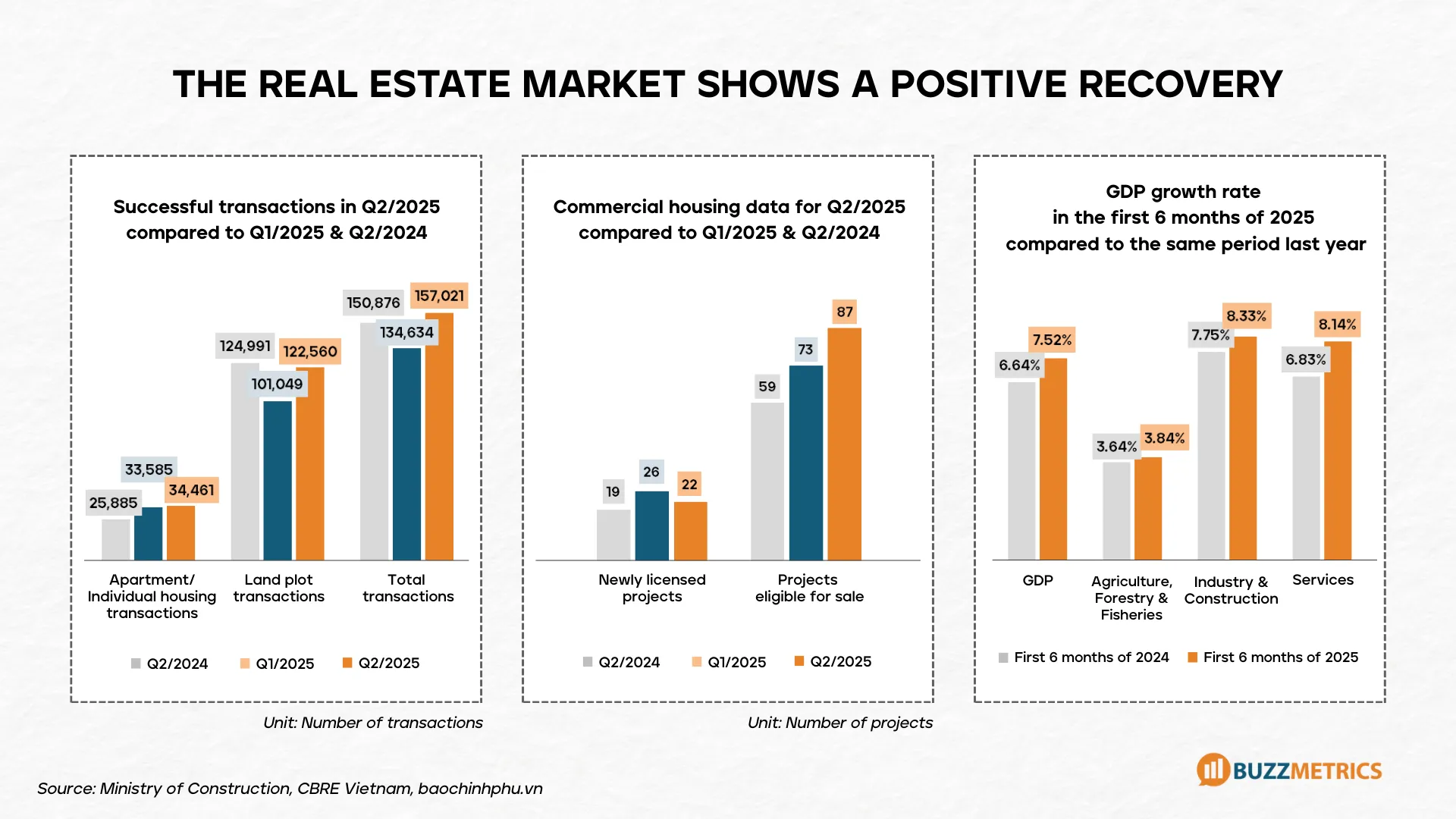

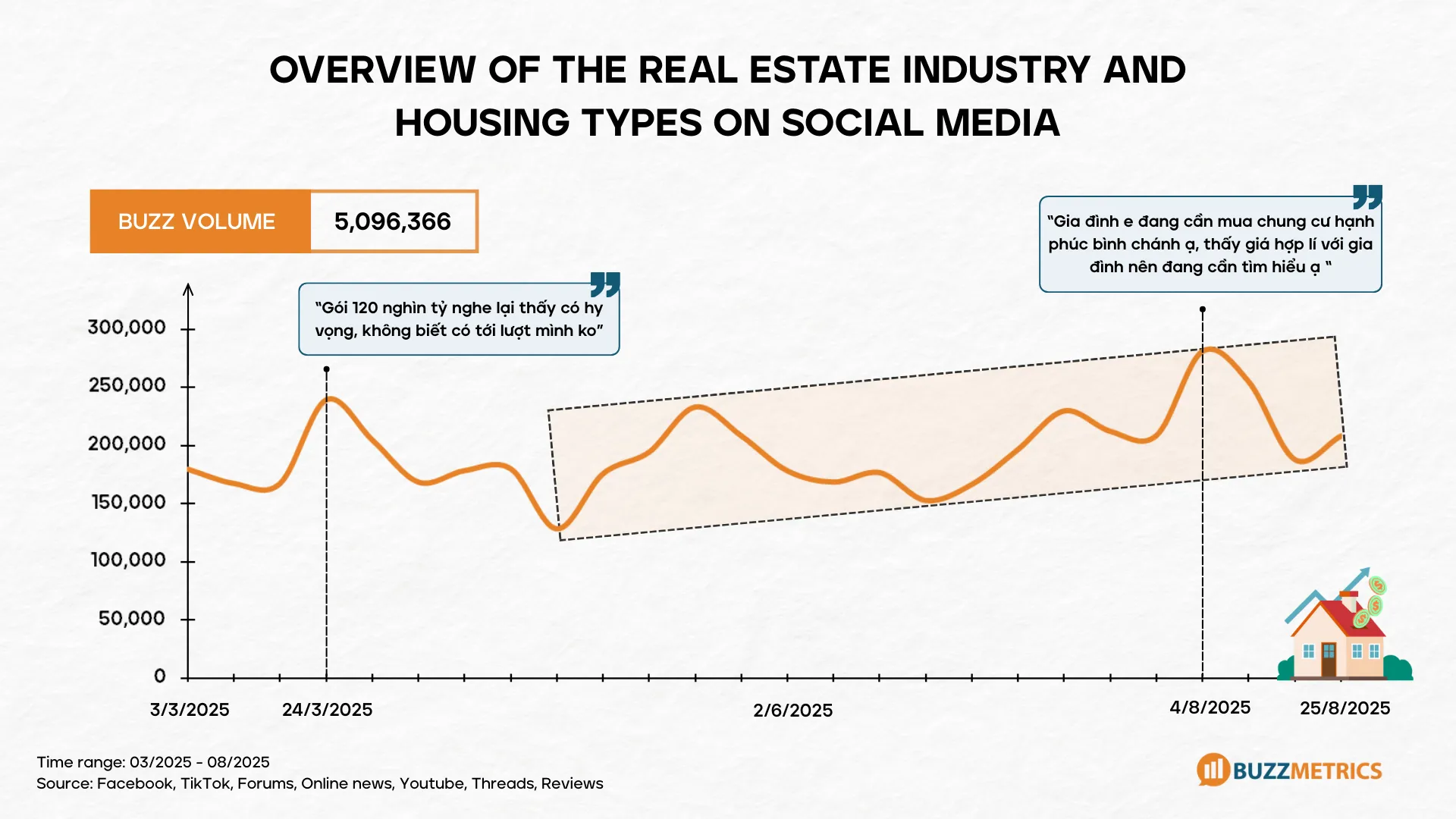

Buzzmetrics’ analysis of Vietnam’s 2025 housing market recorded more than 5 million discussions related to residential real estate in the first six months of the year. This volume indicates that homebuying demand is no longer in a wait-and-see phase; it has shifted into active exploration, comparison, and serious consideration. At the same time, macroeconomic data points to clear signs of recovery: H1 GDP growth reached 7.52%, Q2/2025 transactions increased by more than 20% YoY, and both housing supply and newly approved projects continued to rise. The market is no longer driven by short-term investment expectations, but by genuine end-user demand - especially among young families and first-time buyers.

This article explores three key themes:

➜ For the full dataset, segment-level insights, and how a project like The Felix leverages these signals to improve conversion, refer to the [Báo cáo thị trường nhà ở 2025 – Full Report].

The first half of 2025 recorded 7.52% GDP growth - the highest in 14 years - alongside simultaneous improvements in housing supply, transaction volume, and newly licensed projects. These indicators show not only a warming market but also the return of genuine end-user demand.

Buyer sentiment data reveals that 64% enter the market to live in, while only 36% buy for investment. The three best-performing property types - land plots (33%), apartments (30%), and private houses (21%) - are all closely tied to the need for stable living. Over the next 12 months, apartments and private houses continue to lead interest (31%), showing a shift toward long-term residence rather than short-term speculation.

Since early 2025, three financial policies were loosened simultaneously, quickly reshaping how buyers evaluate affordability:

On social media, these policies are not discussed as macroeconomic updates, but transformed into personal financial equations: “How much do I pay monthly?”, “How does lower interest affect total repayment?”, “Which project truly applies incentives?”

The pace of discussion shows buyers are no longer observing the market from afar; they are actively checking whether new incentives open the door for them to enter.

Adjustments to the Land Law, Housing Law, and the reclassification of merged urban areas are creating new development axes for satellite regions - especially attractive for the mid-range segment (≤ 3 billion VND). Buyers are willing to move farther from the center in exchange for clear legal frameworks, improved infrastructure, and long-term value.

In discussions, buyers focus heavily on areas newly rezoned or proposed to become new urban centers. They no longer view planning as a signal for price growth but evaluate its effect on daily life: commute convenience, school routes, and the potential for a stable residential community.

The first six months of 2025 recorded over 5 million discussions related to residential real estate. Conversations gradually increased and peaked at 281,000 mentions in early August - coinciding with intensified news about credit packages, legal updates, and provincial-city mergers.

The key insight is not the volume, but the shift in discussion content. Buyers are moving from general observation to problem-solving behaviors tied to decision-making: safe loan structures, which policies actually apply, and whether new planning affects commute times or daily convenience. Housing consideration is being shaped by foundational factors: loan capacity, legal clarity, and urban structure - not speculative price expectations.

Beyond typical topics like price, location, and legal status, new discussion themes emerged: comparing bank interest rates, optimizing loan packages, and weighing pros/cons between mid-range apartments and suburban land plots.

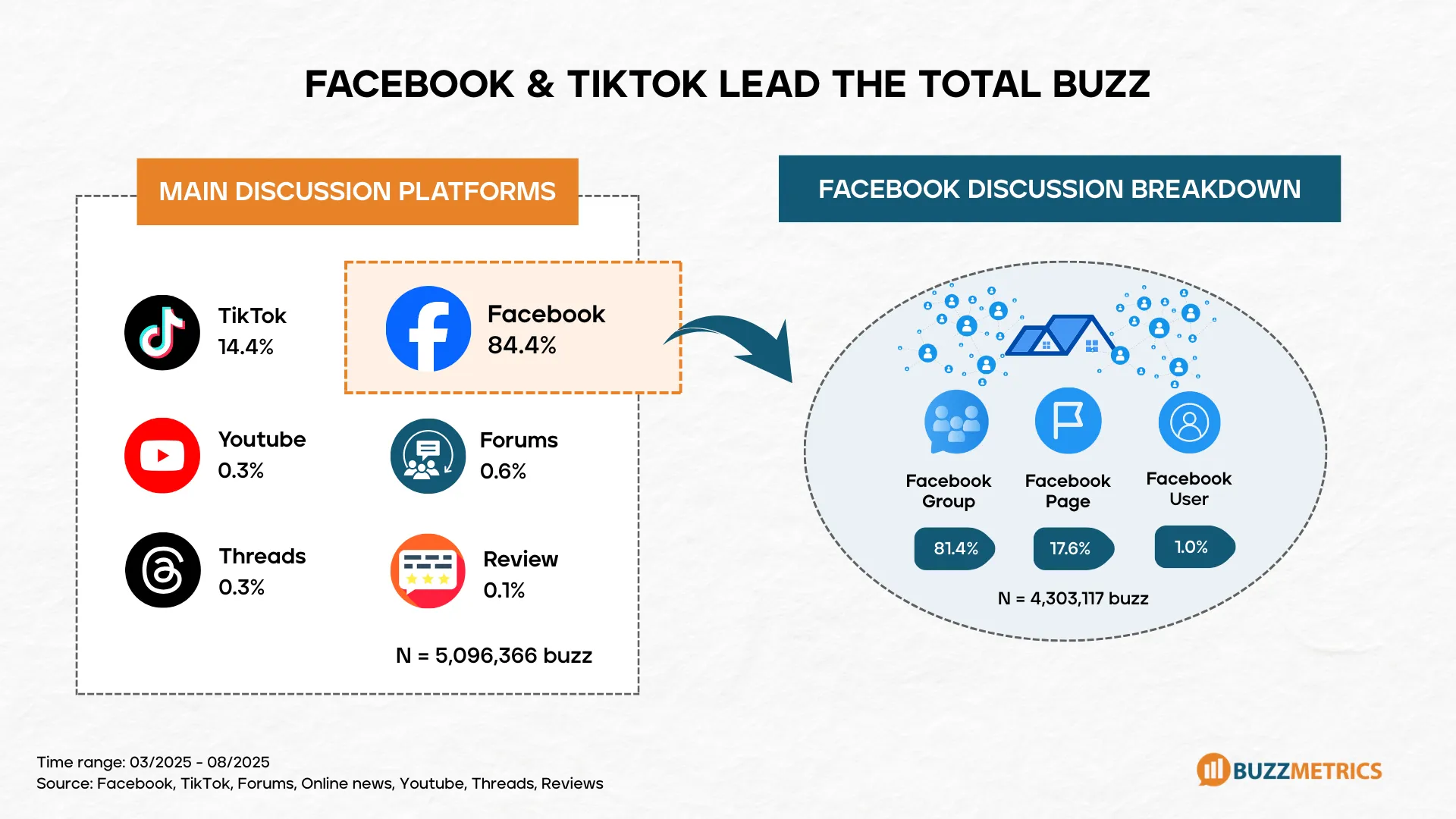

Facebook (84.4%) and TikTok (14.4%) dominate conversations, each taking on distinct roles:

Facebook functions as an ecosystem where buyers ask questions rarely addressed by official channels: handover quality, hidden fees, management responsiveness, safety, or resident conflicts. These real experiences shape expectations and directly influence which projects earn trust or are excluded.

On the contrary, TikTok becomes a “virtual property tour,” where users verify what they’ve heard through visuals: construction progress, landscaping, resident density, mobility experience, and overall liveability. Together, these platforms not only reflect demand but actively shape each step in the buyer’s decision-making process.

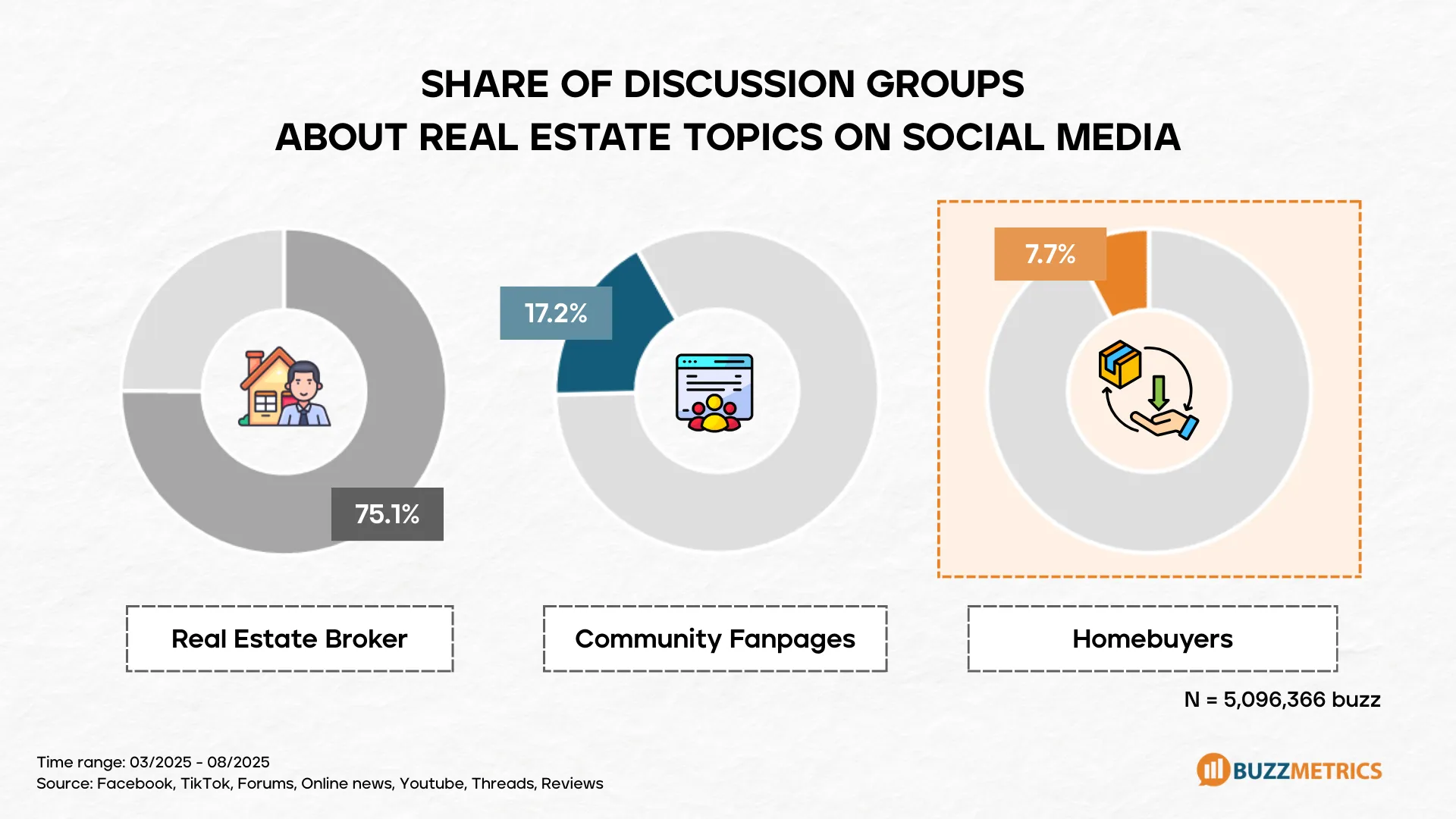

Although brokers still dominate discussions (75.1%), a noteworthy shift is the rise of authentic voices: real buyers and current residents now account for over 20% - the highest in three years. This group is the most trusted, as they reflect lived experience rather than sales-driven narratives.

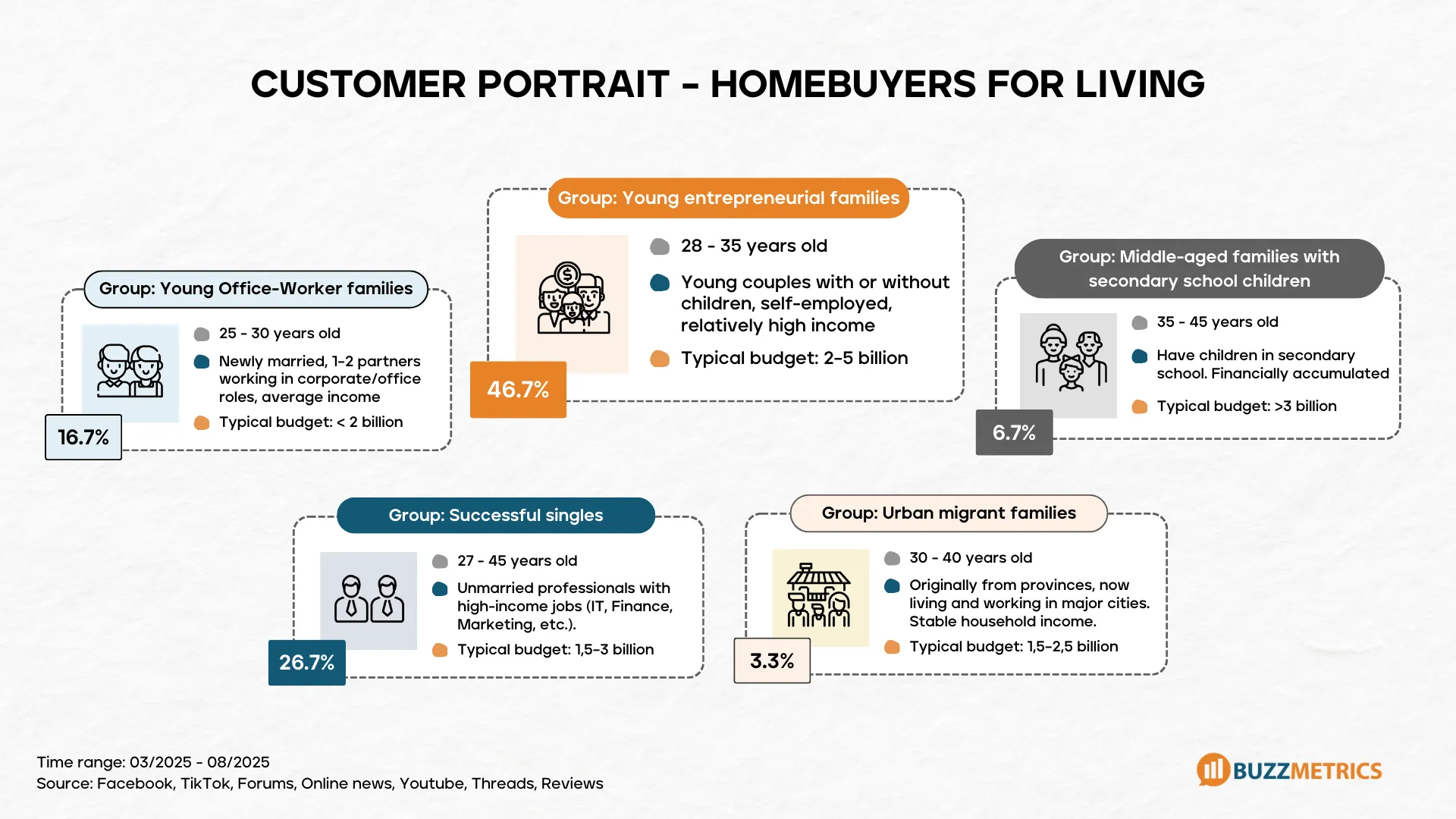

Leading much of the conversation are financially capable young adults - especially small-business families and successful singles aged 23–35. Their budgets center around 2–5 billion VND, aligning with urban living needs and early asset-building goals. A consistent trait of this group is their daily reliance on social media and preference for community validation over broker advice.

Behavioral data shows social media is not just a reference channel but the primary space where buyers form nearly their entire decision, especially during two stages: Information Search and Infomation Ask & Sharing. By 2025, most buyers only meet brokers or visit show units after forming a “preliminary conclusion” on social - a shift not common in previous years.

.webp)

Over 49% of discussions occur in the first stage, showing that buyers turn to social media to establish basic criteria: reasonable price, suitable location, secure legal status, and reliable developers. This is when they start identifying which options are feasible and which risks should be avoided.

The importance of this stage lies not in the amount of information gathered, but in the ability to narrow down choices. When legal risks, slow progress, or unaffordable prices are detected early in discussions, buyers immediately eliminate those projects - helping the journey focus faster.

This initial filtering lays the foundation for the next stage. Once a shortlist is created, buyers begin asking more personalized questions.

This stage accounts for the largest share of discussion (49.6%) and is when buyers reveal their true needs. Conversations shift from general information to project-specific questions: Is the commute feasible during rush hours? Does the unit layout fit a family of 3–4? Are management fees stable? How is the current resident community?

If the Information Search stage filters out unsuitable projects, the Consideration stage filters to find the most suitable ones.

Although only 0.4% of discussions happen at this stage, it serves as a validation rather than an exploration phase. Buyers visit show units to verify the information they’ve collected from social media over the first two stages. Observations - lighting, hallway conditions, finishing quality, and facility operations - are compared against resident feedback, video reviews, and group discussions. If the actual experience aligns with social media insights, the project is added to the final selection. Significant mismatches, however, lead to immediate rejection.

Only 0.6% of discussions occur at the purchase stage, reflecting that the decision is almost entirely shaped in the first two stages. At this point, buyers merely complete the paperwork; the project choice is no longer reconsidered. Social media has already done its job - building trust, narrowing options, and leading buyers to the final decision.

Observing the full discussion journey on social media, several key signals are reshaping how buyers approach the market:

_11zon.webp)

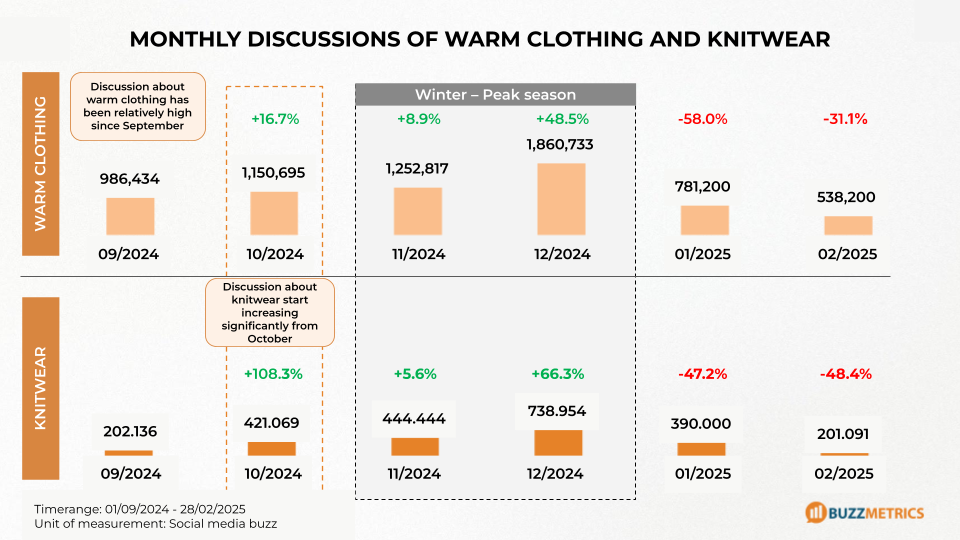

As winter arrives, demand for warm-fashion on social media surges and gives rise to distinct seasonal consumer behaviors. Buzzmetrics research shows that knitwear is not only an essential wardrobe item but has also evolved into an emotionally meaningful product—often chosen to express care for loved ones during the year-end period. This article analyzes social media discussion data and offers content directions to help brands optimize their communications for the peak season.

As early as September, social media users were beginning to stir conversations about warm clothing. However, the real surge only erupted during the November–December period, when mentions of warm apparel peaked at 1.86 million in December (+48.5%).

Notably, knitwear emerged as an unmissable item. Starting in October, discussion of knitwear recorded a record growth of +108.3%, signaling a clear shift in user preferences as people proactively searched for fashion pieces at the onset of colder weather. The appeal of knitwear stayed strong, peaking at nearly 740,000 mentions in December.

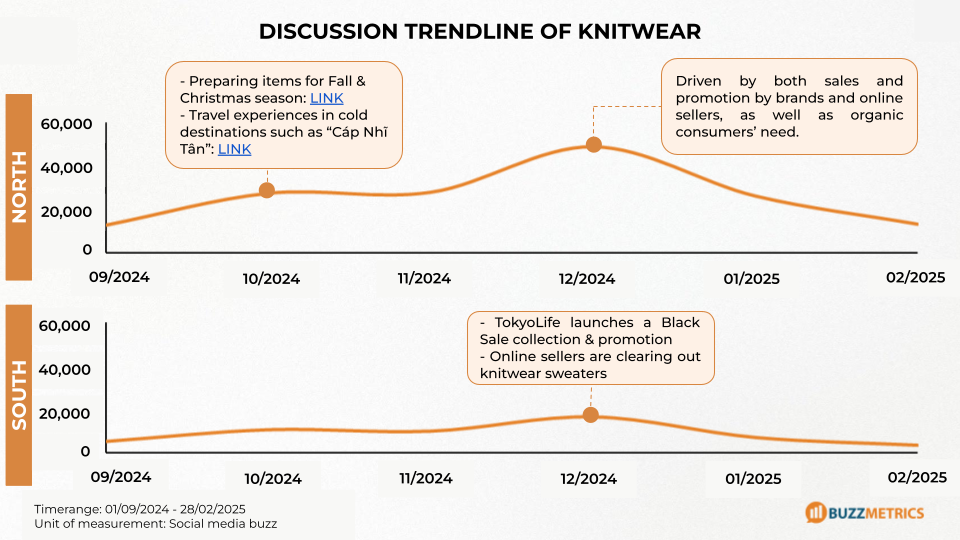

When we dig deeper into discussions about knitwear, the root causes of this “craze” show a clear split: conversations in the North account for the majority of total volume and peaked in December 2024, driven mainly by preparations for the autumn–winter season, Christmas, and shared travel experiences to extremely cold destinations like Harbin (Cáp Nhĩ Tân). By contrast, the peak in the South is smaller and is primarily driven by non-weather factors such as brand promotion campaigns and online retailers’ clearance sales. This suggests that while growth in the North is fueled by practical demand, brands can still spark strong conversations in the South through commercial events and discount campaigns.

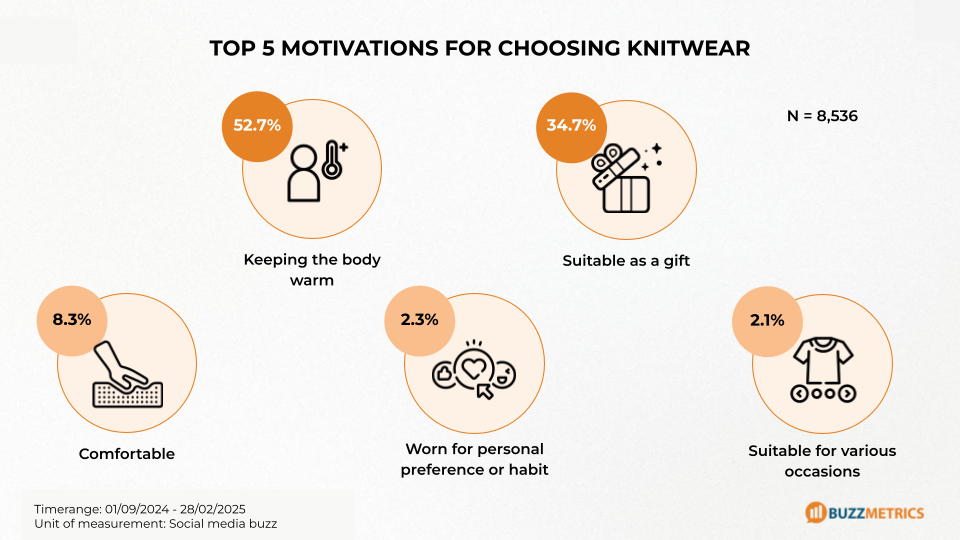

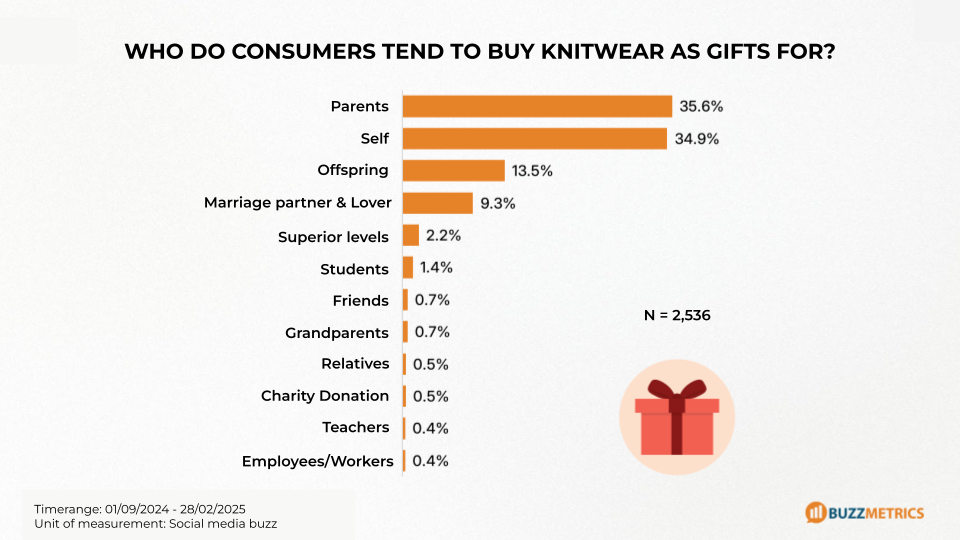

Data shows that conversations related to gift-giving account for 34.7% of all discussions—making it a new growth driver for the knitwear category. Consumers view knitwear as a way to express care and affection, especially toward parents, partners, and loved ones. This presents an opportunity for brands to expand their positioning, shifting from a focus on “warming functionality” to highlighting its “emotional value” during the festive season.

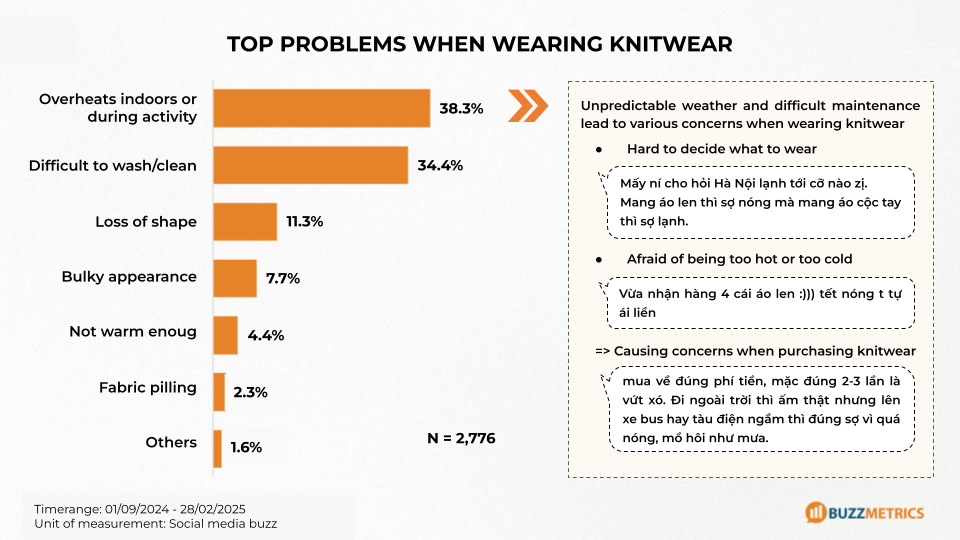

Despite strong purchasing motivation, choosing knitwear still faces major barriers—chief among them unstable weather and the product’s limited adaptability. Among all concerns, “getting too hot indoors or during activities” accounts for 38.3% of discussions, while “difficulty in washing/cleaning” makes up 34.4%. With unpredictable temperature shifts, consumers constantly struggle with the question: “What can I wear that keeps me warm in the early morning but doesn’t overheat me by noon?”. These challenges, combined with worries about stretching and pilling, have created a clear market need: brands must guide consumers toward knitwear options that can flexibly adapt to a variety of weather conditions.

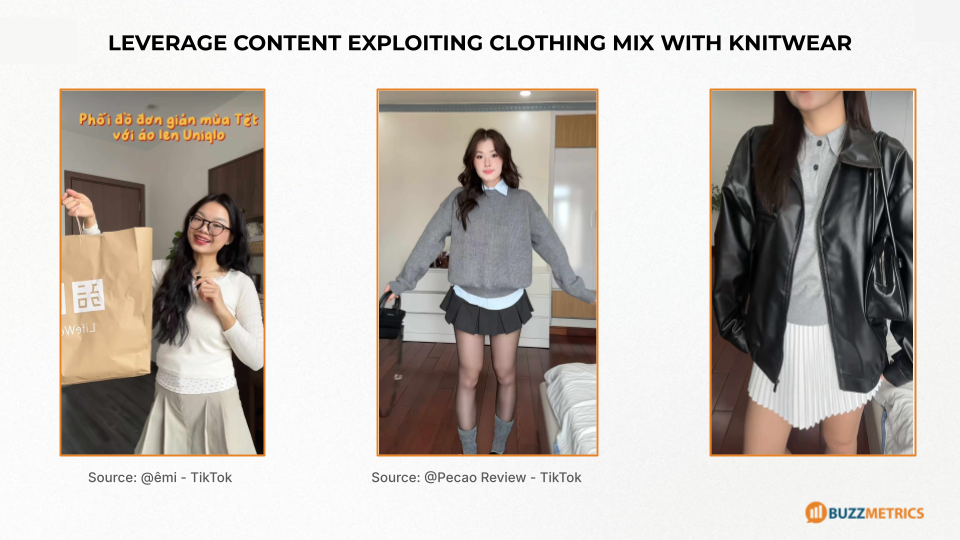

To address the barrier of “difficulty adapting to changing weather,” brands should prioritize solution-oriented content. Instead of showcasing single products, build outfit combinations tailored to specific scenarios: cold mornings–warm afternoons, work–leisure, or extreme-cold travel. The rise of TikTok creates a strong opportunity for Mix & Match videos with KOLs/Reviewers, demonstrating real-life situations and reducing consumer hesitation. For example, major brands like Uniqlo frequently collaborate with TikTok creators such as @emi and @Pecao Review to produce Mix-and-Match style guides.

Data show that gift-giving is not just a passing trend but a key growth driver for the knitwear market, accounting for 34.7% of discussions about purchase motivations. Consumers view knitwear as a way to express care—especially for family members—so brands should shift their messaging from “just keeping warm” to positioning knitwear as a “gift of care”: highlight emotion, gifting stories, and thoughtful gestures instead of focusing solely on functionality.

As another winter approaches, knitwear continues to be a must-have category for every fashion brand. Beyond its warming function, social media data shows a strong emotional driver: knitwear is increasingly seen as an expression of care and affection — a sentiment that now dominates much of the conversation and creates clear commercial opportunities. To capitalize on this shift, brands should:

Gen Alpha is predicted to soon become a core consumer group, driving significant changes in the economy and emerging as a highly promising target audience for brands.

According to McCrindle Research, around 2.6 million children are born every week worldwide, and the Gen Alpha population is expected to exceed 2 billion by the end of 2024. Gen Alpha, or Generation Alpha, is predicted to soon become a core consumer group, driving significant changes in the economy and emerging as a highly promising target audience for brands.

According to a report by DKC, Gen Alpha in the U.S. is estimated to spend approximately $2,340 per year on themselves. The volume of consumer goods attributed to this generation is expected to grow as they gain full autonomy over their purchasing decisions in the future. At present, their influence on consumption is primarily reflected through the purchasing behavior of their parents, mainly from Generation Y. Statistics show that about 49% of Gen Alpha parents are influenced by their children's opinions when making household purchasing decisions.

Meanwhile, Gen Alpha stands out as a generation that grows up alongside technology, much like Gen Z. From birth, their access to technology has been entirely different from previous generations. According to McCrindle Research, items such as the Nokia 1100, landline phones, DVDs, CDs,... have largely disappeared from their world, replaced by iPhones, Apple Watches, AI, 5G,.... From an early age, Gen Alpha has been exposed to emerging technologies as well as social media platforms. As a result, they are often referred to as “digital citizens,” developing in tandem with technology.

Therefore, social media platforms represent a promising space for brands to observe and monitor this generation in a more direct and visual manner. So, what is Gen Alpha in Vietnam doing on social media and what are their defining characteristics? Are there any similarities or differences among Gen Alpha, Gen Y and Gen Z that brands should pay close attention to? Let’s explore more about Gen Alpha in this article!

In addition to insights on Gen Alpha, Buzzmetrics also provides a wide range of market reports across various industries and target customer segments. You can explore more in our Market Insight Library.

Generation Alpha (Gen Alpha) is a demographic term coined by Mark McCrindle to describe children born between 2010 and 2024. He explained that the reason behind the name is that Gen Alpha represents the first generation of the 21st century, a beginning of something new, rather than a return to the old. Therefore, there was no reason to cycle back to the letter A in the Latin alphabet as with previous generations. Hence, the name “Alpha” was chosen, it is the first letter of the Greek alphabet (α), symbolizing the beginning of a new era.

In 2010, the birth year of Gen Alpha also marked the launch of the first iPad and the official debut of Instagram. This is a generation that grows up with technology, able to access information quickly, and is shaped by progressive lifestyles, mindsets, and perceptions.

Because Gen Alpha has been using social media from a very young age, their thoughts and perspectives are also expressed through social media. The Gen Alpha group, aged 9 to 13, already has an independent voice on social media.

Gen Alpha has established an independent voice on social media early on. Their interaction style online shares many similarities with both Gen Z and Gen Y, as all three generations enjoy engaging through comments on fanpages and online groups. Among these, fanpages see the highest interaction rates (73.9% for Gen Alpha, 80.7% for Gen Z, and 64.4% for Gen Y).

However, when examining discussion behavior in more detail, each generation possesses its own distinct characteristics. Specifically, Gen Alpha and Gen Y tend to prefer creating content on social media, in contrast, Gen Z is more inclined to follow existing content.

(+) On personal pages, Gen Alpha and Gen Y tend to create original posts more often, while Gen Z prefers to comment on or share posts from other platforms. If one tries to understand Gen Z’s lifestyle based solely on their personal pages, it may be difficult, whereas the opposite is true for Gen Alpha and Gen Y.

(+) In groups, Gen Alpha and Gen Z mainly prefer to engage through comments. For Gen Y, in addition to commenting, creating their own posts is also a common form of interaction.

At first glance, Gen Alpha might seem to share similar discussion platforms with Gen Z. However, the top fanpages that attract the most engagement from Gen Alpha are quite different. Specifically, in addition to general information pages like “Cao thủ” and “Theanh28 Entertainment”, Gen Alpha also actively engages in discussions on pages focused on love topics (Luv Sad) and gaming (“Liên Minh Huyền Thoại: Tốc Chiến”). Moreover, the top five most popular discussion channels among Gen Alpha do not include astrology-themed pages, unlike those favored by Gen Z.

As for Gen Y, their interests are not as unified as those of Gen Alpha and Gen Z, but rather dispersed across different subgroups. However, social news pages still attract significant attention across most of these groups, notably “Chửi Thuê”, “Theanh28 Entertainment” and “Hóng Hớt Showbiz”,...

Although Gen Alpha has only recently joined social media, data collected from 300 Facebook discussions shows some of their key interests. Similar to Gen Z, Gen Alpha prioritizes three main topics: emotions, memes, and idols. In contrast, the topics that Gen Y is interested in are quite different from those of Gen Alpha and Gen Z. This generation is more segmented into smaller groups with varied interests. For instance, single individuals tend to focus more on social news or romantic relationships, while those with children are primarily concerned with parenting topics.

Delving deeper into the data reveals an interesting insight, although Gen Alpha is still of school age, discussions related to education account for only 7.3%.

(+) Romantic Topics: Among Gen Alpha, romantic topics receive the most attention. Discussions often revolve around finding a partner, expressing emotions, and raising questions about love. For instance: "Why are we online but not texting each other?" or "Once you genuinely like someone, it's hard to stop..."

(+) Meme Topics: Meme remain a hot topic for both Gen Z and Gen Alpha. However, each generation has distinct preferences. Gen Alpha prefers using meme that feature screenshots of text messages and real people. In contrast, Gen Z tends to favor animal meme and meme from iconic animated series like Tom & Jerry, as well as Disney and Ghibli films.

Gen Alpha has already begun making their first moves on social media. In the next 3-5 years, they are expected to become an important customer group for brand development, thanks to their active presence on social platforms.

This customer group will share many similarities with Gen Z, as both generations grew up alongside technological advancements. However, the data reveals some distinct differences in the platforms and discussion topics favored by each generation, reflecting their unique interests and characteristics.

Most members of Gen Alpha are being raised by parents from the Millennial and Gen Z. Discussions around the topic of parenting from these two generations reveal more open-minded and distinct perspectives compared to previous generations. This suggests that Gen Alpha’s values, interests, and ways of self-expression will carry many unique traits.

Today, Gen Alpha has become a key customer segment for several industries. As a result, brands are already beginning to research and monitor the behavior and psychology of this generation, especially on social media in order to take timely and appropriate steps to stay ahead.

For a long time, Millennials have been considered the main consumer force by brands due to their strong purchasing power and continuous growth over the years. However, this generation is now showing signs of being caught up by a completely new generation: Gen Z. According to Nielsen, by 2025 in Vietnam, Gen Z is expected to reach 15 million people and account for 30% of the consumer base.

Even now, brands tend to focus more on Millennials and there is still a lack of research on Gen Z. When it comes to Gen Z, brands often do not have a clear image, instead associating the generation with keywords like young, creative and active on social media. However, Gen Z’s actual behavior on social media differs from how brands currently perceive them. So, what is Gen Z really like? Let’s explore in the article below with Buzzmetrics.

The age range for Gen Z is different in each country, but most agree that this generation includes those born between 1997 and 2012. Unlike the young people of Gen X and even Gen Y, Gen Z grew up with digital technology from an early age, becoming familiar with the Internet and social media and mastering smart devices even before they could read or write. As a result, this generation is also known by various other names: iGeneration, Generation, Homeland, Net Gen, Neo-Digital Natives, Digital Natives, Pluralist Generation, Internet Generation, Centennials, Later - Millennials, Gen Wii, Zoomers, Gen-Tech,…

When mentioning Gen Z, we often think of a young group still in school and not yet financially independent, which leads to limited purchasing power and mainly influencing their parents' buying decisions rather than being the final decision-makers themselves. However, in reality, the oldest members of Gen Z are now between 24 and 27 years old. They are already working, financially capable and some have even started families of their own.

According to research by McKinsey, Gen Z currently accounts for 40% of global consumers. Additionally, Nielsen’s study titled “Generation Z - The consumers of the future” found that over 70% of surveyed Gen Z individuals reported having a significant influence on their family’s purchasing and lifestyle decisions. This includes decisions related to outdoor activities, entertainment, household items, clothing, food and beverages.

These figures highlight Gen Z as a highly promising consumer group with growing purchasing power. As a result, brands around the world are beginning to recognize that this generation is simply too important to ignore. A report by The Influencer Marketing Factory revealed that 97% of Gen Z admit that social media influences their shopping decisions. Additionally, a separate study by Statista found that 54% of Gen Z believe social media helps them discover new products more effectively than traditional online search methods.

Given these insights, it’s clear that to engage Gen Z effectively, brands must gain a deep understanding of their digital behavior, especially on social media platforms.

The digital environment has become an essential part of Gen Z’s daily life. Because of their close connection with the virtual world, brands often view Gen Z as content creators on social media, who actively express opinions or share reviews online.

However, according to Buzzmetrics, Gen Z is more likely to engage with content more than create it. They prefer engaging with others' posts (by liking, commenting or sharing) rather than creating their own. If they do post something, it’s usually a selfie accompanied by a simple caption. Questions like “What does Gen Z care about?” or “What is their lifestyle like?” are difficult to answer just by looking at their personal pages. In contrast, older generations such as Gen X or even some Millennials are often more willing to create content, writing posts to express their opinions (about family, society, lifestyle, etc.) or to share everyday activities (like travel, leisure, shopping). Their interests and lifestyle choices are often clearly reflected on their social media profiles. This presents an interesting contrast, as older generations are often referred to as Digital Immigrants. They grew up before social media existed and are usually seen as less tech-savvy. Yet, the way they present themselves online tends to be more open than Gen Z. As a result, in order to truly understand and connect with Gen Z, brands must identify where this generation genuinely belongs in the digital space.

Key questions:

Sign up to purchase the Gen Z report here.

Gen Z is a young generation that has grown up immersed in technology and has helped expand the vocabulary of social media users. You’ll often come across comments that include quirky phrases like “dảk dảk” or “bủh bủh” - signature expressions of Gen Z’s online language. This gives the impression that any space on social media could be a buzzing discussion spot for them. However, research from Buzzmetrics shows a different side: this group tends not to share much about their personal lives through food photos or selfies with short captions. In other words, their personal profiles often appear relatively quiet, which challenges the common assumption that Gen Z is always present and vocal everywhere online. So where exactly does Gen Z really live on social media?

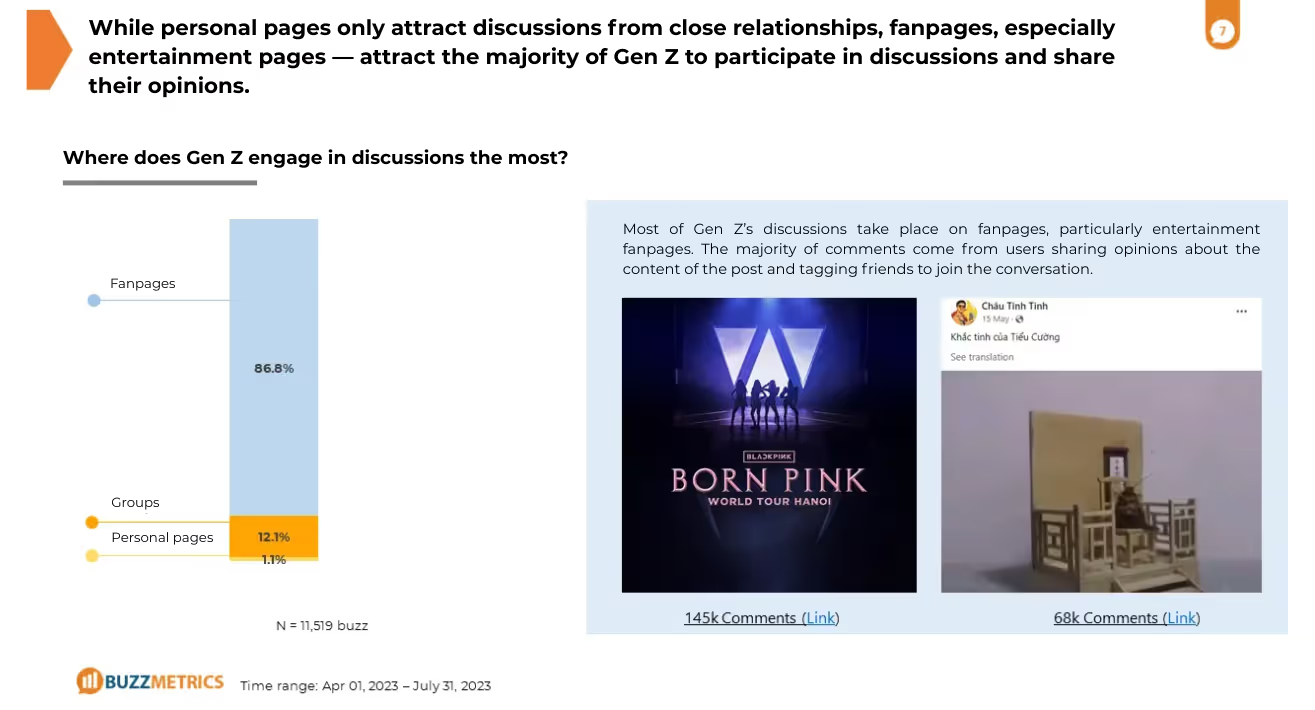

According to Buzzmetrics’ research on social media discussions, Gen Z tends to share and engage in public conversations less on their personal profiles and more on channels with a stronger community focus such as fanpage. Specifically:

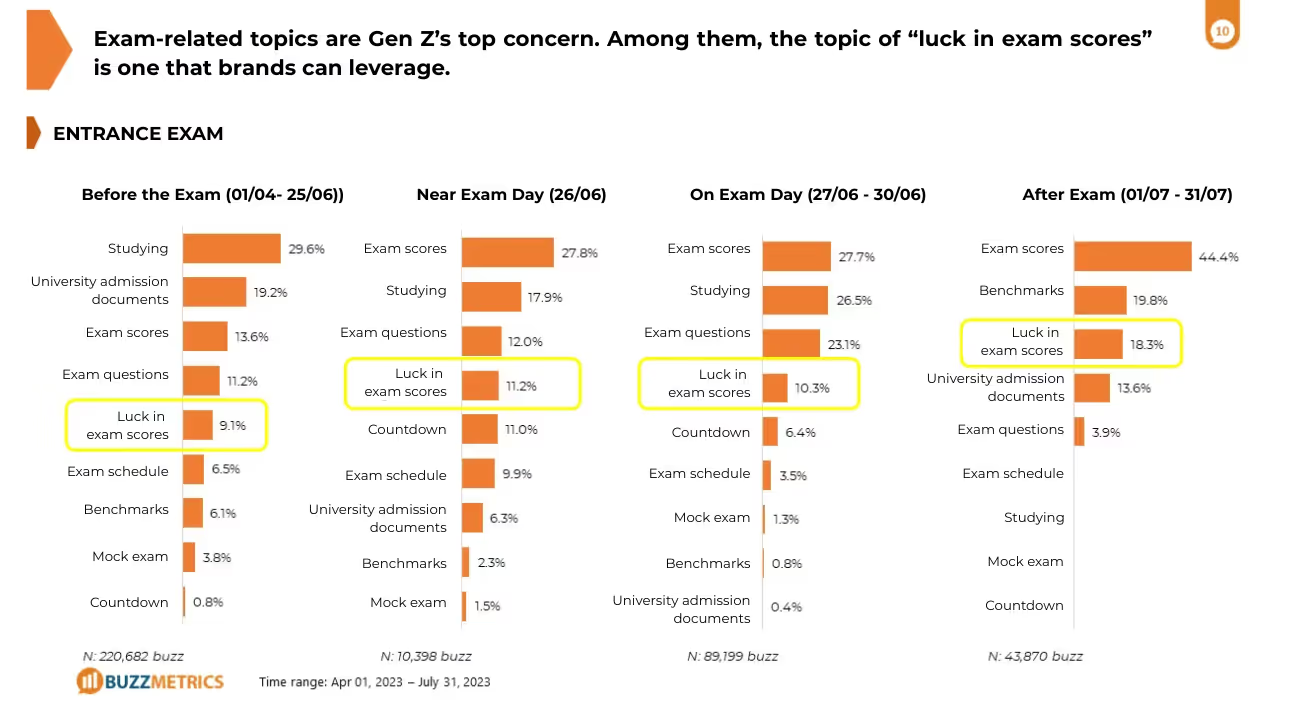

Gen Z discusses differently on community pages compared to their personal pages. Compared to previous generations, Gen Z has often been portrayed by the media as a mysterious generation. This is not only because Gen Z is relatively new and less thoroughly studied, but also because their true interests can only be identified by tracking discussions in community channels. There are topics considered “exclusive” to Gen Z, most notably school and exams. Among these, content about “luck” in exams presents an opportunity for brands to explore more deeply.

In the context of exam-related stress and anxiety, the element of luck is often valued by Gen Z students, sometimes even serving as an important source of emotional encouragement. Brands can take advantage of this topic by creating spiritually themed content like “share a spoon to get high scores” to boost engagement.

Aside from school-related topics, love and football are also subjects that Gen Z pays special attention to.

Read more: Euro 2024 through the lens of Social Listening

Key questions:

Register to purchase the Gen Z report here.

→ See also: What is target audience research?

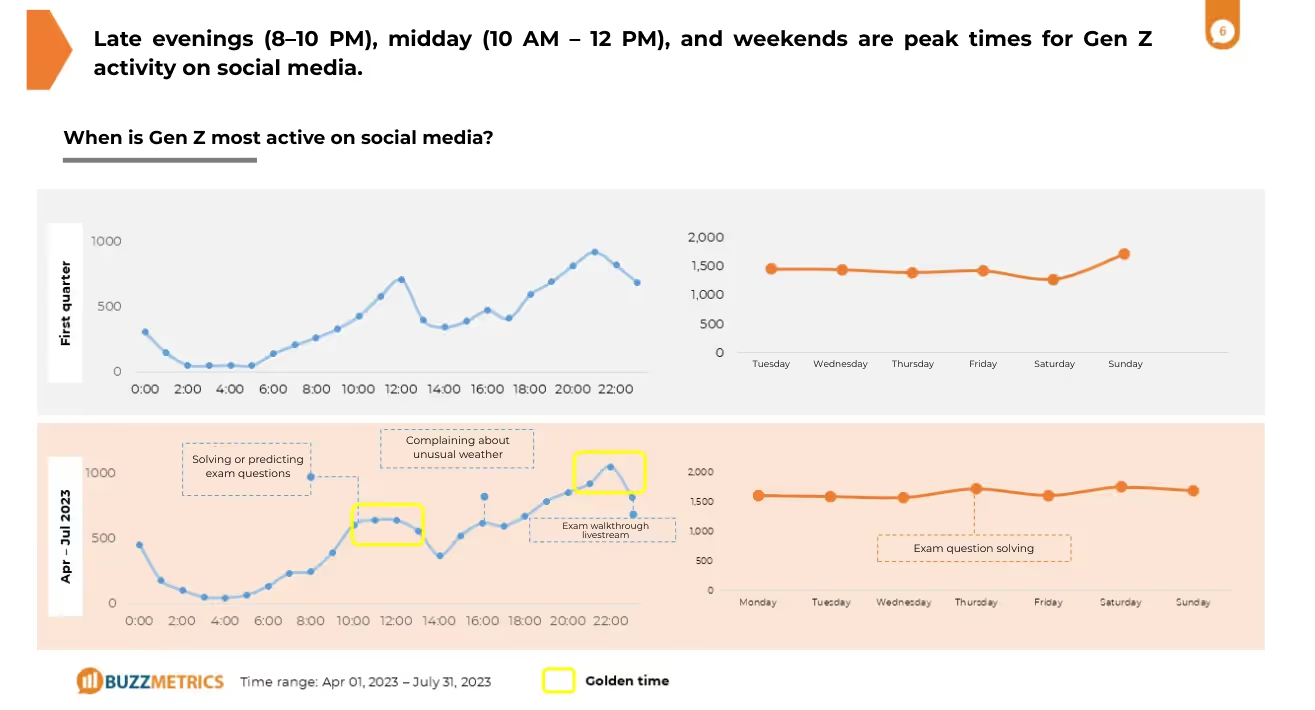

Understanding the peak activity times of Gen Z on social media helps brands optimize post timing, run ads or organize online events to effectively reach this audience.

To seize opportunities and boost sales from Gen Z, brands must clearly understand the behavior of this group on social media. By choosing the right timing, creating content and products that accurately reflect what Gen Z wants, marketing campaigns will achieve greater effectiveness, leading to sustainable business growth.

Leverage the right relevant topics: Understanding and leveraging the topics that Gen Z cares about most will help brands create viral content and enhance their reach on social media. When it comes to entertainment content, the content strategy of Gimbap 178 Minh Cầu is a notable example. While the entire F&B industry focuses on posting food photos, Gimbap 178 Minh Cầu skips that trend entirely and instead emphasizes meme content - short, humorous posts with little commercial intent. Their posts still revolve around food but are presented from quirky, humorous angles that attract Gen Z. The brand also posts consistently at 5 PM. This regular posting of memes helped build a habit among Gen Z of "checking in" on social media at that time, thereby boosting interaction frequency with the brand.